By: Udaibir Das

This article originally appeared in OMFIF on April 9, 2026.

Structural transformation in banking persists well beyond the disruption

Banking systems do not merely weaken under conflict. They are structurally transformed. Yet this institutional dimension – how banking itself is reorganised under conflict – remains largely absent from the policy debate. Under conditions of armed conflict and state rupture, banking shifts away from decentralised intermediation towards directed, survival-orientated finance. Market allocation weakens, state priorities dominate and the changes persist long after the disruption ends. Yet the policy conversation has concentrated on sanctions, commodities and trade – the institutional reorganisation of banking under conflict remains less well examined.

Banking systems are the primary channel through which macroeconomic damage under conflict is transmitted. Research in the International Monetary Fund’s April 2026 World Economic Outlook shows that output in conflict-affected economies falls cumulatively by roughly 7% within five years – losses that exceed those from financial crises or severe natural disasters and that persist a decade later. Public debt rises by up to 14% of gross domestic product during wartime. Yet the mechanism itself – how banking is rewired under conflict – remains poorly understood.

What economic history reveals

The historical record is remarkably consistent. Work by the National Bureau of Economic Research documented this transformation in real time during the second world war. Banks were converted from commercial intermediaries into instruments of sovereign finance: interest rates were suppressed, credit was directed and balance sheets became concentrated in government paper. In the UK, the Bank of England’s holdings of government securities rose to £62.6m by November 1918 from £11m in July 1914 – to 33% from 13% of total assets. The pattern extends further back: research on the Napoleonic period shows the Bank of England supporting wartime borrowing through liquidity provision and managed debt issuance, while evidence from the seven years’ war points to short-term crowding out of private credit followed by longer-run financial deepening.

What followed was equally consequential. Across advanced economies, financial repression – interest-rate caps, capital controls, directed lending and a tighter government-bank nexus – liquidated public debt at roughly 3% to 4% of GDP per year in the UK and the US between 1945 and 1980. Real rates were negative roughly half the time. In the UK, the cash ratio was formalised in 1946, and a liquidity requirement was introduced in 1951, steering banks towards government paper for decades. The saver, pension fund and depositor all paid the bill.

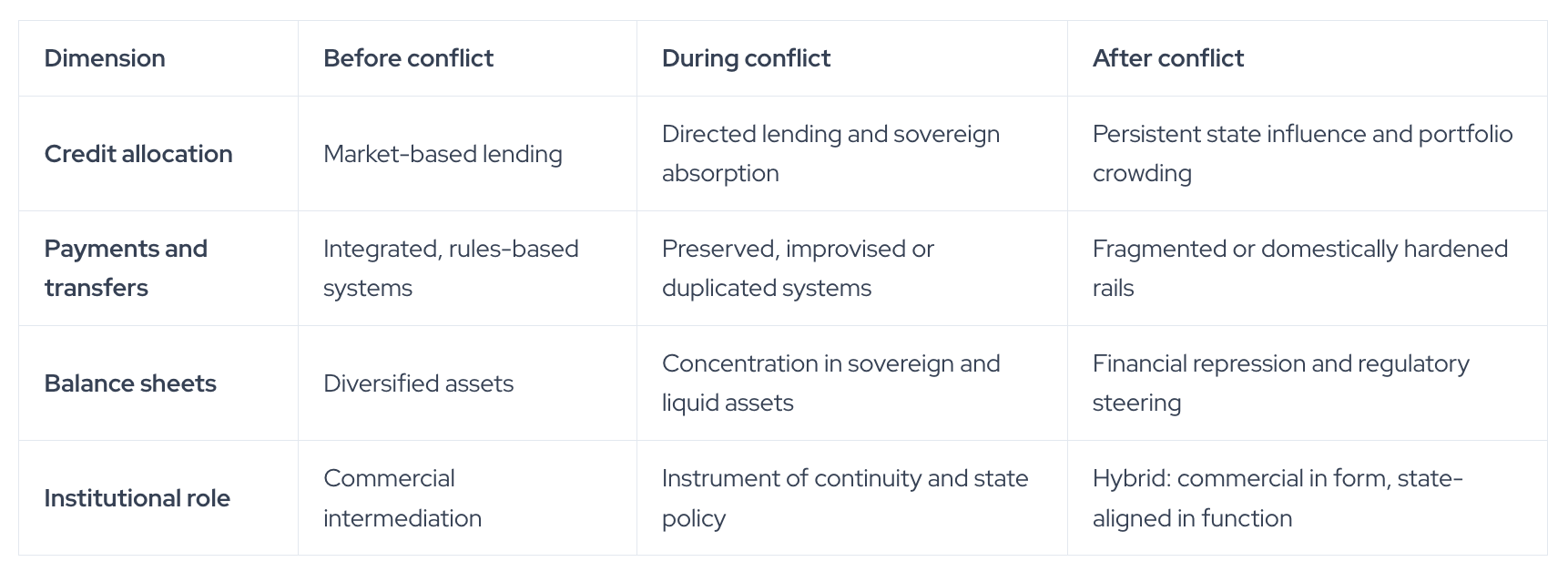

Figure 1. Four dimensions of rewiring

Before, during and after conflict

Source: Author’s framework

Recent experience confirms the pattern – and reveals that the rewiring is not only institutional but behavioural. Households respond to conflict by withdrawing deposits, hoarding cash and shifting savings into foreign currencies or digital assets. Depositors and banks move in the same direction: towards precaution, away from intermediation.

Kuwait after 1990 illustrates the balance-sheet consequences. The 1992 debt-settlement programme transferred large volumes of impaired loans from banks to the state in exchange for government bonds. Banks emerged with stronger capital positions, but at the cost of shifting private losses onto the sovereign.

In Ukraine, asset quality deteriorated rapidly following the 2022 invasion. Banks remained profitable in 2023, largely through central bank instruments and margin expansion rather than broad-based lending, while the authorities prioritised payments continuity through pre-designed operational resilience. The credit channel contracted sharply. The payments channel was actively preserved.

In fragile and conflict-affected states, this pattern becomes persistent. Formal banking narrows while payments, remittances and household transactions migrate to mobile money, cash networks and informal transfer systems. In several settings, mobile money volumes now exceed formal bank transfers many times over. The formal system does not disappear – it hollows out, retaining the regulatory architecture while losing the economic substance. The result is not collapse but bifurcation.

The conflict in the Middle East and the associated oil production crisis introduces a further dimension: the direct targeting of financial centres as theatres of insecurity. Major international banks have evacuated or restricted access to their offices. The threat is no longer limited to borders and boundaries but also to financial hubs.

Technology is altering the form of this adjustment without changing its logic. Digital payment rails, mobile money and stable-value digital instruments expand the channels through which transactions continue when formal banking is impaired. Reports from blockchain analytics firms indicate that stablecoin flows linked to conflict-affected economies surged markedly during 2025.

Regarding the conflict, reports suggest that stablecoins have been used at scale – by state institutions to settle trade and by ordinary citizens to protect savings as national currencies depreciate. Disruption may not reduce financial activity as much as relocate it – across borders, beyond regulated balance sheets and into systems only partially visible to supervisors.

The evidence – historical and contemporary – points to a consistent pattern. The policy response has not kept pace.

Three practical conclusions could follow

First, central banks and systemic risk authorities could benefit from an operational framework for conflict and geopolitical disruption. Not merely a financial stability contingency plan but a pre-designed architecture for payments continuity, emergency liquidity provision and collateral management under physical disruption. Recent experience, notably in Ukraine, has demonstrated that pre-designed resilience works. Improvisation would not have.

Second, financial and market regulators must treat the sovereign-bank loop as a geopolitical transmission channel. Banks hold sovereign debt; sovereign distress weakens bank balance sheets; weakened banks, in turn, raise sovereign borrowing costs further. This loop has persisted for decades. Regulatory and prudential frameworks must account for it.

Third, post-conflict planning must confront the reconstruction gap. Rebuilding requires long-duration project finance – infrastructure, housing, energy – spanning 10- to 30-year horizons. But banks emerging from conflict hold shortened balance sheets, impaired capital and portfolios concentrated in sovereign paper. Development finance institutions, multilateral lenders and governments will need to provide the long-duration capital that banking systems rewired for survival cannot. The instruments must be created now.

Banks, in such conditions, are not simply private intermediaries. They are part of the national continuity infrastructure. Once rewiring begins, it does not reverse when the disruption ends. It becomes the new operating structure. The question is no longer whether policy frameworks need updating. It is whether they can be redesigned while conflicts are still reshaping the systems they are meant to govern.

Udaibir Das is a Visiting Professor at the National Council of Applied Economic Research, a Senior Non-Resident Adviser at the Bank of England, a Senior Adviser of the International Forum for Sovereign Wealth Funds, and a Distinguished Fellow at the Observer Research Foundation America.