By: Udaibir Das

This article originally appeared in OMFIF on April 21, 2026.

Three reports, one constraint – the sovereignty premium, repriced

The International Monetary Fund’s flagships – the World Economic Outlook, the Global Financial Stability Report and the Fiscal Monitor – are designed to be read in sequence: growth, then finance, then fiscal. This April, they only make sense when read together.

Fiscal space, financial space and institutional credibility are no longer separable policy domains. They are jointly binding constraints. The price at which that constraint settles is what I call the ‘sovereignty premium’ – not merely the cost of default risk, but the price markets assign to a sovereign’s ability to exercise policy autonomy amid tightening fiscal and financial conditions within an international financial system under strain.

That price is rising. The IMF flagships document their components but not the mechanism.

Conflict has become a baseline, not a tail

The WEO’s Chapter 3 is the most analytically ambitious of the three. Using post-1945 data, it estimates that output in conflict-affected economies falls by about 3% at the onset and accumulates losses of roughly 7% within five years, with scars still visible a decade later. These losses exceed those from financial crises and severe natural disasters. Even where peace holds, output typically recovers only about half the observed loss within five years.

Chapter 2 on defence spending completes the picture. Booms have become more frequent, especially in emerging markets. A typical episode raises defence outlays by about 2.7 percentage points of gross domestic product over two and a half years, two-thirds deficit-financed. Fiscal deficits deteriorate by roughly 2.6pp, public debt rises by around 7pp within three years and external balances weaken. Wartime dynamics are sharper: public debt rises by about 14pp and social spending falls.

These are not episodic shocks. They are parameters. Conflict is no longer a tail risk; it is a baseline condition with identifiable balance-sheet effects. Yet debt sustainability frameworks, reserve adequacy metrics and sovereign ratings methodologies still treat it as a qualitative adjustment. This is the first gap between what the IMF flagships see and what the IMF toolkit prices.

Fiscal space has quietly disappeared

The Fiscal Monitor delivers the most consequential single finding of the meetings. The global fiscal gap – the distance between projected primary balances and those required to stabilise debt – has closed. A decade ago, it exceeded 1% of GDP. It is now close to zero.

Global gross government debt reached 93.9% of GDP in 2025 and is projected to approach 100% by 2029, levels last seen in the aftermath of the second world war. The composition is shifting. Interest payments have risen from about 2% to nearly 3% of global GDP in four years. The US is running a general government deficit of 7%–8% of GDP despite operating near capacity, with gross debt projected to reach around 142% by 2031. China’s debt is projected to approach 127%. Global debt-at-risk three years ahead stands near 117% of GDP, with a widening right tail.

What has disappeared is not headline space but optionality. Fiscal policy now enters each new shock with less capacity to respond than it had at the start of the last one. The stock has become a flow problem. The causal chain shortens and the feedback loop tightens. Fiscal choices now shape financial conditions directly, rather than indirectly through growth.

The plumbing has changed, and credibility is the residual

The GFSR is the report that has travelled furthest in a single cycle. Its core analytical move is to relocate sovereign risk from the borrower’s balance sheet to the investor’s. As central banks unwind their balance sheets, private, often leveraged investors have become the marginal buyers of government bonds. Within the non-bank investor base that now dominates emerging market portfolio flows, hedge funds, investment funds and passive vehicles are the most risk sensitive. Their behaviour tracks global conditions more than domestic fundamentals. Countries reliant on these investors face tighter financial conditions during periods of stress that do not cleanly correlate with their own macroeconomic position.

The GFSR names an erosion of the US Treasury’s safety premium. The reference asset of the global financial system is repricing. It also flags a weakening of the equity-bond hedging relationship under more frequent supply shocks, raising the risk of simultaneous selloffs. Movements in US yields now spill over rapidly to other markets, disproportionately affecting economies reliant on external financing.

Transmission accelerates, differentiation collapses. In this configuration, credibility becomes the residual variable. The WEO links pressure on central bank independence to higher inflation expectations; the Fiscal Monitor identifies similar pressures as capable of raising sovereign risk premia even for highly rated economies; the GFSR prices both through investor behaviour. Institutional quality is no longer a background condition. It is the pricing mechanism.

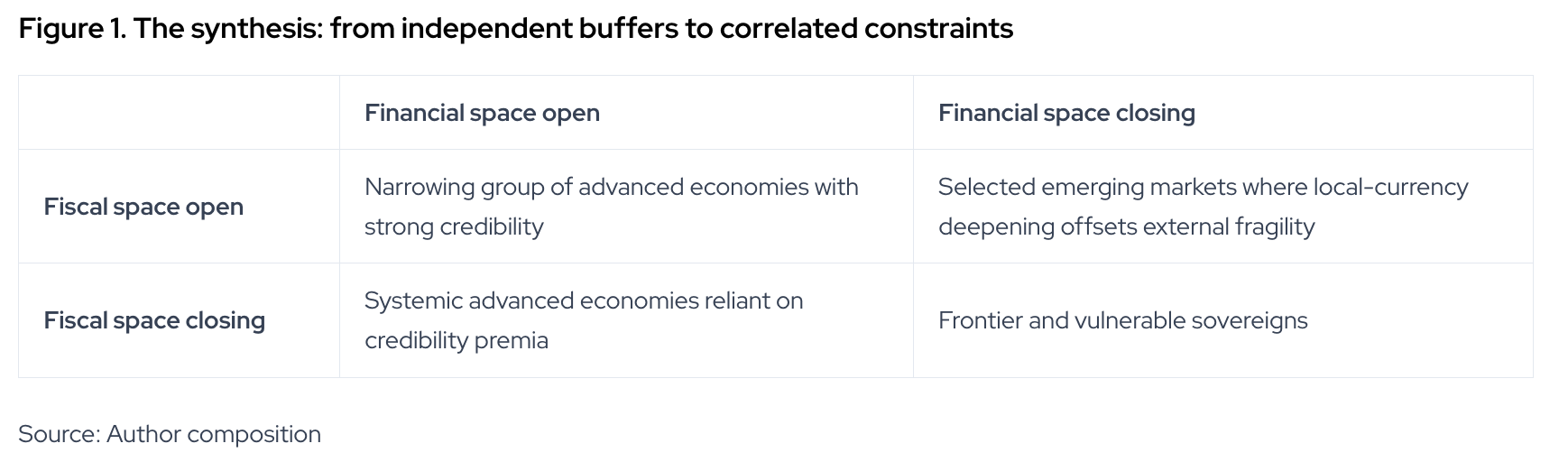

Figure 1 is not a static map. Movement across cells is driven by three variables: the cost of funding, the composition of the investor base and shifts in institutional credibility. What distinguishes the current configuration from a decade ago is the speed and correlation of movement. A tightening in financial conditions now feeds directly into fiscal constraints; a weakening in credibility accelerates both. The bottom-left quadrant – large economies with limited fiscal space sustained by credibility – is where systemic risk now sits. The premium that holds it in place is not unlimited. It can reprice without a prior deterioration in fiscal arithmetic.

The sovereignty premium, repriced

This is where the IMF analysis reaches a boundary it does not cross. The defence burden is the fiscal cost of strategic autonomy. The leveraged marginal buyer reflects the financial cost of dependence on external funding. The eroding Treasury safety premium is the credibility cost at the system’s core. Each is measured. None is connected.

The connection is the sovereignty premium.

Three consequences follow. The debt sustainability framework measures what borrowing costs without measuring what it buys. The deployment gap – the distance between the cost of capital and the developmental return it generates – is the missing asset-side counterpart that the framework lacks. Without it, debt sustainability analysis cannot distinguish borrowing that builds state capacity from borrowing that merely defers constraint.

Capital account openness is no longer a choice between integration and isolation. When leveraged non-banks set the marginal price of government paper, the exchange rate and the yield curve become the joint settlement mechanism for sovereign autonomy. The price is reset continuously by investors whose horizons differ from those of the borrowing sovereign.

Credibility is not exogenous. States are engineering around it, deepening local currency investor bases, building parallel payment systems, reprogramming money through central bank digital currencies and accumulating reserves beyond traditional adequacy metrics. It is architectural control. The state reconstitutes its position in the financial system at a price of autonomy different from the one set by global markets. The IMF’s instruments do not yet capture this third mode. They treat the sovereignty premium as noise around a liberal baseline. In April 2026, it is the signal.

What follows for surveillance

The IMF’s forthcoming Comprehensive Surveillance Review – the periodic reassessment of how the IMF conducts bilateral and multilateral surveillance under Article IV – is the moment to translate these findings into instruments.

Conflict must enter core frameworks, not sit alongside them. Investor composition must enter external and financial assessments; the behaviour of the marginal buyer now matters as much as aggregate flows. The disappearance of fiscal space requires sharper country-level guidance. The constraint is systemic, but the resolution is national. And the sovereignty premium belongs in the analytical toolkit. Surveillance that does not price the cost of autonomy cannot advise on its management.

The April 2026 IMF flagships describe a system in which buffers no longer operate independently, policy space is jointly constrained and the reference asset is repriced. The analysis is there. The frameworks have not caught up. The lexicon is still missing.

The sovereignty premium is now the price at which the global financial system transacts with the sovereigns that fund it. That price is rising. Whether it reprices gradually or abruptly is now the only question that matters.

Udaibir Das is a Visiting Professor at the National Council of Applied Economic Research, a Senior Non-Resident Adviser at the Bank of England, a Senior Adviser of the International Forum for Sovereign Wealth Funds, and a Distinguished Fellow at the Observer Research Foundation America.