Special report no. 10

BY PIYUSH VERMA, caroline arkalji, AND TELMEN ALTANSHAGAI

I. CONTEXT AND STRATEGIC LANDSCAPE

The global steel industry sits at the center of the industrial transition to a low-carbon economy. Steel is the backbone of modern infrastructure, supporting construction, transportation, energy systems, and manufacturing. Yet it is also one of the most carbon-intensive industrial sectors, accounting for roughly 11 percent of global carbon dioxide emissions. The sector also represents a significant pillar of the global economy, contributing an estimated 3 percent to 4 percent of global gross domestic product and underpinning critical industries such as transportation, construction, electrical equipment, and manufacturing.

As global demand for infrastructure, electric vehicles, renewable energy systems, and urban development continues to grow, steel production is projected to rise significantly over the coming decades. In 2024, global steel production exceeded 1.8 billion metric tons, and demand is projected to reach nearly 2 billion tons annually by 2030 and 2.5 billion tons by 2050, driven largely by rapid economic growth in India, Southeast Asia, and parts of Africa. Meeting climate goals while sustaining this demand presents one of the most complex challenges in the global energy transition. According to the International Energy Agency, emissions from the sector must fall by roughly half by mid-century to remain consistent with global climate objectives.

The geography of this transition is overwhelmingly concentrated in Asia, which today hosts roughly 80 percent of global blast furnace capacity and the vast majority of newly announced steelmaking projects. China alone produces more than half of the world's steel and accounts for the largest share of sectoral emissions, while India is emerging as the fastest-growing major steel market and remains significantly more carbon intensive, emitting about 20 percent to 25 percent more CO₂ per ton than China. Together, China, India, Japan, Russia, and South Korea account for nearly 80 percent of global steel-related greenhouse gas emissions, meaning that policy and investment decisions across these economies will largely determine the trajectory of the sector's decarbonization. At the same time, export-oriented producers such as Japan and South Korea face growing exposure to emerging climate-related trade measures and carbon-conscious markets. Together, the policy choices, investment strategies, and technological pathways adopted across Asia will play a decisive role in the decarbonization of the global steel sector.

Technological pathways for reducing emissions are increasingly visible. Steelmakers across the world are exploring hydrogen-based direct reduction, advanced electric arc furnaces (EAF) using scrap steel, and carbon capture technologies. However, scaling these solutions requires far more than technological innovation. The transition demands enormous volumes of low-cost clean electricity, new hydrogen supply chains, high-quality iron ore inputs, and entirely new infrastructure systems. According to the Mission Possible Partnership Steel Transition Strategy, reaching a net-zero compliant steel sector by 2050 would require approximately $170-$200 billion in annual investment, 52-75 million tons of hydrogen per year, and an additional 5,700-6,700 terawatt-hours of electricity per year. Meeting these requirements will increasingly depend on the development of integrated industrial hubs where renewable power, hydrogen production, ironmaking, and steel manufacturing are co-located to reduce costs and infrastructure bottlenecks. As a result, the transformation of steelmaking is increasingly tied to the restructuring of energy systems, industrial supply chains, and international trade relationships.

Discussions at a recent ORF America international convening in Seoul emphasized that technological feasibility is no longer the central barrier to steel decarbonization. Instead, the challenge lies in achieving alignment at the system level across energy systems, industrial supply chains, and trade frameworks. Large-scale decarbonization will depend on how energy systems, market structures, and geopolitical dynamics evolve together, particularly in areas such as scrap availability and hydrogen deployment. While greater alignment around definitions of "green steel" can help reduce transaction costs and improve market transparency, it alone cannot drive investment or create demand. In this context, fragmented policy frameworks, weak demand signals, and high capital costs remain key constraints on large-scale deployment.

The coming decade will be decisive as steel demand continues to expand, particularly in emerging economies. India, for example, illustrates the scale of this shift. Supported by strong domestic demand, large infrastructure investments, and favorable industrial policy, the country's steel consumption is projected to grow by 5 percent to 6 percent annually, reaching 240-260 million metric tons by 2035. Installed crude steel capacity, currently around 180 million metric tons, is expected to rise to 260-280 million metric tons over the same period. Yet, much of this expansion is likely to rely on blast furnace-basic oxygen furnace (BF-BOF) production, raising the risk of new carbon-intensive assets being locked in for decades.

At the same time, India has structural energy dependencies, as it relies on imports for the majority of its metallurgical coal, estimated at around 90 percent, which, in turn, raises energy security concerns and the risks of building a steel system anchored in externally sourced fossil inputs. This dependence also exposes the sector to price volatility and supply chain disruption, reinforcing the importance of diversifying input sources and accelerating the development of alternative production routes over the long term.

These dynamics are not unique to India but reflect broader patterns across many emerging steel-producing economies, where rapid demand growth, existing infrastructure, and energy dependencies shape the trajectory of the sector. Whether the industry can move from pilot projects to industrial transformation will depend on coordinated action across governments, producers, investors, and end-use industries, particularly in aligning energy systems, financing frameworks, and demand signals. Therefore, steel decarbonization is not only a climate challenge but also a question of industrial competitiveness, energy security, and global economic leadership.

II. STEEL DECARBONIZATION REQUIRES COORDINATED GLOBAL MARKETS

Decarbonizing the global steel industry is often framed primarily as a technological challenge. While innovation in hydrogen-based ironmaking, EAFs, and carbon capture is essential, the central constraint facing the sector today is increasingly economic and institutional rather than technological. Steel decarbonization therefore reflects the scale of transformation required across markets, supply chains, and policy frameworks, shaped by investment risks, cost structures, and global trade dynamics.

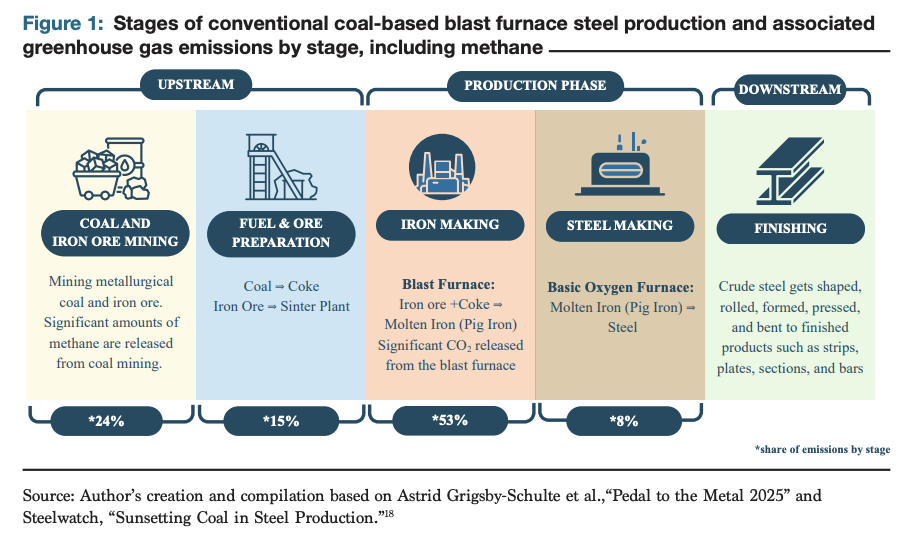

A key structural factor is the concentration of emissions in the ironmaking stage of steel production, as illustrated in Figure 1. The traditional BF-BOF route relies on metallurgical coal both as a fuel and as a reducing agent to convert iron ore into iron, making it the most emissions-intensive stage of the process.

Although lower-carbon production routes such as emerging hydrogen-based direct reduced iron (DRI) and long-established scrap-based EAFs can significantly cut emissions, the global steel system remains dominated by coal-based BF-BOF infrastructure. This reflects structural constraints, including the limited availability of high-quality scrap for EAF production, high and volatile electricity costs, and the continued reliance on existing coal-based assets. Roughly two-thirds of global steel production capacity continues to rely on BF-BOF technology, much of it concentrated in Asia.

This technological lock-in is reinforced by the long lifespans of steelmaking assets. Blast furnaces and associated infrastructure operate for around 40 years, creating strong incentives for producers to maximize the economic return on existing investments rather than retire them prematurely. Over this period, furnaces undergo major relining every 15–20 years to extend their operational life, at a cost equivalent to 25 percent to 50 percent of building a new blast furnace. These reinvestment cycles create narrow decision windows during which low-emission technologies can be adopted, and choices made at these points can lock in production pathways for decades. As a result, decisions around replacing or retrofitting steel plants carry significant financial risks, particularly in emerging economies where steel demand continues to grow rapidly.

Cost Competitiveness as a Key Constraint

Cost competitiveness further complicates the transition. Low-emissions production routes often require significantly higher capital investment and access to large volumes of low-cost clean electricity or hydrogen. Energy and raw material costs alone can account for 60 percent to 80 percent of overall steel production costs, meaning that even modest changes in input prices can significantly alter competitiveness. The resulting cost difference between conventional and low-emissions steel production, often referred to as the “green premium,” remains a major barrier to large-scale deployment.

Existing market structures have struggled to generate reliable demand signals for green steel, limiting incentives for producers to invest in low carbon production pathways. While some early demand side initiatives have emerged, particularly in Europe, including binding offtake agreements such as the partnership between Volvo Cars and Swedish steel company SSAB to supply near-zero emissions steel for serial vehicle production, these efforts remain geographically concentrated and limited in scale. In contrast, the majority of global steel production capacity is in Asia, creating a mismatch between where demand signals are emerging and where production is concentrated.

Traditional labeling or taxonomy approaches have not yet translated into a consistent premium market in which customers are willing to pay for lower-emissions materials. At the same time, producers face operational challenges in gradually transitioning blast furnace assets while maintaining supply commitments to customers who require steel from specific production facilities. Emerging mechanisms such as chain-of-custody certification systems, which track and verify how inputs and associated emissions data move through each stage of the supply chain, may help address this constraint by enabling the transfer of emissions reduction value to downstream buyers. In addition, mass balance accounting approaches are being advanced in countries such as Japan. These systems allow low and high emissions inputs to be physically mixed, while allocating emissions reductions to specific outputs through certified accounting. Industry guidelines pool emissions reductions at the company level and allocate them to selected products, supported by emerging policy frameworks to help scale early markets for low carbon steel.

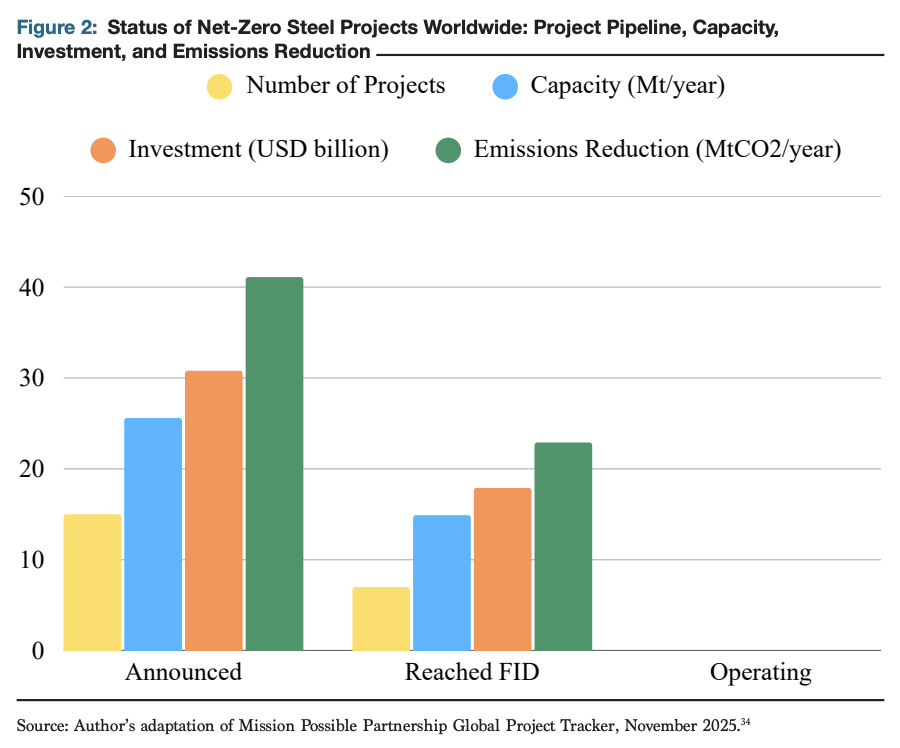

Global investment trends further illustrate the scale of the challenge. While more than 1,000 commercial-scale clean industrial plants have been announced across energy-intensive sectors such as chemicals, aviation, aluminum, and steel, only sixty-two have reached final investment decision (FID), and just eighty-two are currently operational and producing final products. The gap is even more pronounced in the steel sector. Only twenty-two projects are currently under development globally, of which fifteen are awaiting investment decisions, with seven have reached FID. None are operational at this time. China is leading the world in these projects, accounting for five of the twenty-two total projects capable of 70–80 percent emissions reductions across the full production process compared to conventional routes. This reflects not only the role of consistent policy signals, but also substantial state support and public financing, which help de-risk capital-intensive investments and accelerate project development.

However, these project pipelines remain limited compared to the global steel industry. In 2024, global crude steel production was about 1.885 billion tons. Reaching a 1.5 degrees Celsius-aligned, net-zero steel sector would require about 170 million tons each year of near-zero-emissions primary steel production by 2030. However, only seven projects have reached the final investment decision, representing just 14.9 million tons each year. Projects at FID therefore account for less than 1 percent of current global steel production, highlighting the gap between ambition and deployment.

These dynamics highlight the importance of aligning demand signals, certification systems, and financing structures to enable the scaling of low-emissions steel production. Without credible market signals and mechanisms to bridge the green premium, investment in new production pathways is likely to remain limited.

III. FRAGMENTED STANDARDS AND TRADE RISKS

As governments and industries decarbonize steel production, an equally complex challenge is the governance of green steel markets. The transition is unfolding in a policy environment characterized by differing standards, certification systems, and trade measures across regions. Without greater alignment on definitions, monitoring systems, and regulatory frameworks, fragmented markets for low-emissions steel run the risks of slowing investment and complicating international trade.

At the same time, the steel sector operates within highly competitive global markets that are increasingly shaped by a combination of climate, trade, and industrial policy measures. Policies such as the European Union's Carbon Border Adjustment Mechanism (CBAM), emerging carbon markets in countries such as India, and shifting tariff regimes in the United States and other major economies add new layers of uncertainty to investment decisions by introducing evolving emissions thresholds, compliance requirements, and carbon cost exposures, as well as changes in trade conditions and market access that affect long-term competitiveness.

A central issue is the absence of universally accepted definitions of what constitutes "green" or low-emissions steel. Countries and organizations are developing their own taxonomies and certification frameworks, often reflecting domestic industrial priorities and technological pathways. India, for example, recently introduced one of the world's first national green steel certification systems, which evaluates emissions performance both at the plant level and for individual steel products. While such initiatives represent important progress, differing methodologies and thresholds across jurisdictions may create inconsistencies that complicate international trade and supply chain transparency.

Credible monitoring, reporting, and verification (MRV) systems are becoming a critical foundation for the development of global green steel markets. Robust MRV frameworks provide the "common ground" necessary to build trust in emissions claims and enable cross-border transactions in low-emissions materials. South Korea, which established the first national emissions trading scheme in Asia, brings significant institutional experience that could help advance interoperable regional standards and data systems. However, the effectiveness of such systems continues to be debated, particularly regarding the continued allocation of free emissions allowances to energy-intensive industries such as steel. Analysts argue that this may weaken effective carbon price signals and reduce incentives for emissions reductions. Even with these concerns, the need for greater alignment remains clear. Establishing comparable metrics for emissions intensity, certification procedures, and product labeling will be essential in allowing producers and buyers across different markets to transact with confidence.

Trade policy is further reshaping the incentives facing steel producers. The European Union's CBAM entered its operational phase in January 2026, applying the EU's carbon price to imports of emissions-intensive goods such as steel. Furthermore, the European Commission has proposed strengthening the mechanism by expanding its scope to around 180 steel- and aluminum-intensive downstream products, with implementation expected from January 2028. By effectively applying the EU's domestic carbon price to imports, CBAM aims to prevent carbon leakage and protect European industry from competition with higher emissions producers. However, it also creates new pressures for exporters, particularly in Asia, to reduce the carbon intensity of their steel production to maintain access to European markets. At the same time, it may strengthen demand for lower-emissions steel and improve the competitiveness of producers that are able to meet these standards.

For export-oriented economies such as Japan and South Korea, these measures introduce additional strategic considerations. Steel producers must navigate evolving regulatory environments while maintaining competitiveness in highly globalized supply chains. Concurrently, geopolitical dynamics create a fluid market environment. Recent developments, including anti-dumping duties imposed by South Korea on hot-rolled steel plates imported from Japan and China and ongoing adjustments to tariffs and industrial policies in major economies, illustrate how rapidly changing trade dynamics can influence investment decisions across the sector.

The complexity of the steel supply chain further amplifies these challenges. Steel production relies on globally distributed inputs, particularly iron ore supplied by major exporters such as Australia and Brazil. These countries play a critical role in the upstream segment of the steel value chain and are increasingly exploring opportunities to shift toward producing low-carbon iron products such as DRI or hot briquetted iron (HBI) that can feed emerging green steel markets. However, without harmonized standards and certification frameworks, differences in regulatory regimes could fragment global markets, creating parallel supply chains and increasing compliance costs for producers and exporters.

These developments highlight a central risk of fragmentation in the global steel trade. If regulatory frameworks, certification systems, and trade policies continue to evolve independently across jurisdictions, the result could be increasingly fragmented markets for green steel. Aligning standards, strengthening MRV systems, and coordinating policy approaches will therefore be essential in ensuring that the transition to low-emissions steel supports rather than disrupts global industrial cooperation.

IV. TECHNOLOGY PATHWAYS ARE EMERGING — BUT CLEAN ENERGY SCALING REMAINS DIFFICULT

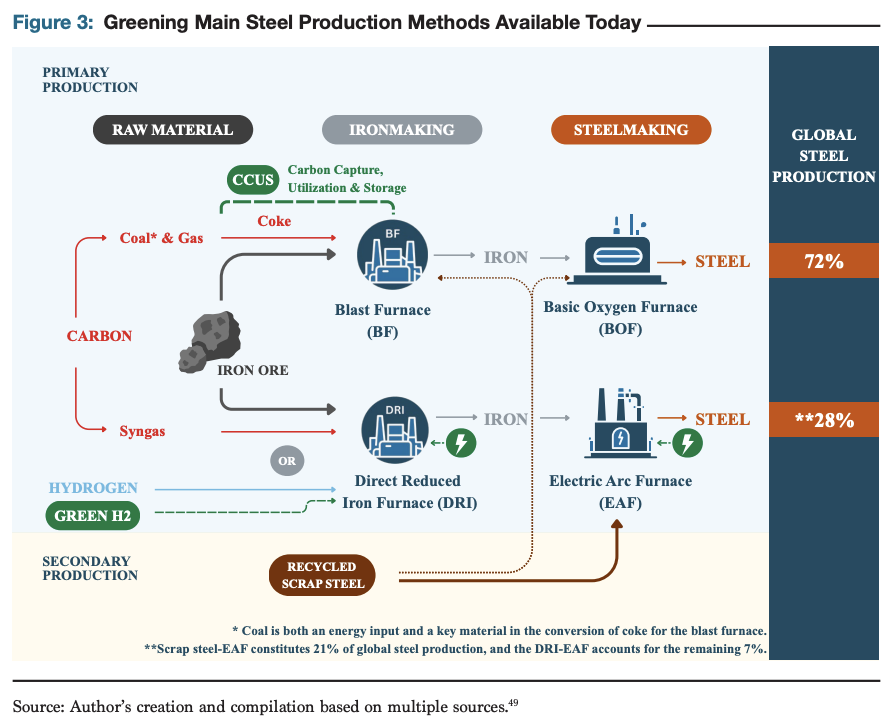

Steel production broadly follows two main routes: primary steelmaking, which produces iron from iron ore before converting it into steel, and secondary steelmaking, which relies primarily on recycled scrap steel. Three production pathways dominate global output, each with different energy emissions intensities. The BF-BOF route remains the most prevalent, accounting for roughly 72 percent of global steel production. Scrap-based electric arc furnace (scrap-EAF) production represents about 21 percent, while direct reduced iron combined with electric arc furnaces (DRI-EAF) accounts for roughly 7 percent.

Within this system, technological options for reducing emissions in the steel sector become increasingly clear. As illustrated in Figure 3, hydrogen-based direct reduction, expanded use of electric arc furnaces through greater steel recycling, and carbon capture technologies are all being explored by producers across the world. However, the central constraint facing these pathways is not the maturity of steelmaking technologies themselves, but the broader energy and infrastructure systems required to support them. Decarbonizing steel therefore requires parallel transformation across electrical systems, hydrogen supply chains, and industrial infrastructure.

The energy system has effectively become the "binding constraint" for green steel deployment. Low-emissions production routes require enormous volumes of reliable and cost-competitive clean electricity. Renewable energy will be a critical enabler of this transition, yet its availability, cost, and intermittency also create major operational challenges for energy-intensive industrial processes such as steelmaking. A single large-scale green steel plant producing approximately 5 million tons annually can require as much as 20 terawatt-hours of electricity each year, nearly ten times the demand of Sweden's largest existing industrial facilities, such as aluminum smelters and mechanical pulp mills. Scaling hydrogen-based steel production therefore demands rapid expansion of renewable generation capacity, major upgrades to transmission grids, and new industrial infrastructure capable of transporting hydrogen and storing captured carbon dioxide.

Among the available technological pathways, expanding EAF production based on recycled steel scrap represents the most immediately deployable option. Scrap-based steel-making bypasses the highly emissions-intensive ironmaking stage and can significantly reduce the sector's carbon footprint, particularly when powered by low-carbon electricity. However, the potential for this pathway is constrained by the limited availability of high-quality steel scrap and the technical requirements of certain high-grade steel products, particularly those required in the automotive industry. In addition, the economics of EAF production are sensitive to electricity prices, and in countries such as South Korea, relatively high and volatile power costs can significantly reduce margins and limit its competitiveness. While scrap recycling already plays an important role in global steel production, current scrap supply is insufficient to meet projected demand. Combined with constraints related to electricity costs, this limits the scalability of EAF-based production, meaning that primary ironmaking processes will continue to dominate global steel production for decades.

Hydrogen-based DRI is widely viewed as the most promising long-term pathway for near-zero emissions steelmaking. By replacing coal with hydrogen to remove oxygen from iron ore, the process can significantly reduce emissions, particularly when the hydrogen is produced through electrolysis powered by renewable electricity, often referred to as green hydrogen. Electrolysis requires substantial energy input, typically around 50-55 kilo-watt-hours of electricity to produce one kilogram of hydrogen, making the cost of clean electricity a decisive factor in the economics of hydrogen-based steelmaking. At present, most hydrogen used globally is produced through steam methane reforming (SMR) of natural gas, commonly referred to as grey hydrogen. This typically costs $1.60-$2 per kilogram but generates significant carbon emissions. When carbon capture is added to produce blue hydrogen, costs rise to approximately $2.10-$2.20 per kilogram.

Producing green hydrogen remains considerably more expensive, with costs varying widely across regions, from below $6 per kilogram in areas with abundant low-cost renewable energy, such as parts of the Middle East, China, India, and Australia, to as high as $8-$10 per kilogram in higher cost markets such as Central Europe, reflecting differences in resource availability and electricity prices. However, costs have already fallen significantly, by roughly 60 percent over the past decade, and are expected to decline further as electrolyzer manufacturing scales up and renewable electricity prices continue to fall. By 2030, green hydrogen costs could reach as low as $3 per kilogram in favorable locations such as India or China.

At current prices, replacing coal with hydrogen could increase the cost of producing a ton of steel by roughly one-third, creating a major barrier to widespread adoption. Over time, this gap may narrow as renewable electricity becomes cheaper and carbon pricing raises the cost of coal-based production, though many estimates suggest hydrogen prices would ultimately need to fall to $1-$1.50 per kilogram for hydrogen-based ironmaking to compete with conventional blast furnace routes.

Feedstock constraints pose an additional challenge for hydrogen-based DRI. The process requires high-grade iron ore pallets, at least 67 percent iron, with low concentrations of impurities. Because hydrogen reduces iron oxides but does not remove impurities, strict feedstock quality is necessary to maintain reduction efficiency and stable furnace operation.

Yet only a small share of global iron ore supply meets this threshold. Estimates suggest that less than 4 percent of currently mined ore qualifies as direct-reduction grade without further upgrading. Large-scale adoption could therefore reshape iron ore markets by increasing demand for high-grade ores as well as for beneficiation technologies capable of upgrading lower-grade resources. At the same time, alternative production routes capable of processing lower-quality ores into green DRI, such as NeoSmelt and HyREX, are being explored, although these technologies remain at an early stage of development.

Carbon capture, utilization, and storage (CCUS) has been proposed as another pathway to reduce emissions from existing blast furnace infrastructure. While CCUS for coal-based blast furnaces could play a transitional role for facilities that cannot easily shift to alternative production routes, its long-term viability remains uncertain. Current carbon capture technologies cannot fully eliminate emissions, and large-scale deployment depends heavily on the availability of CO2 transport infrastructure and suitable geological storage sites. Despite repeated attempts, the CCUS has had limited success in the steel sector, with only one commercial-scale facility, the Al Reyadah plant in the United Arab Emirates, capturing around 25 percent of emissions, and no similar projects deployed since.

High costs and infrastructure constraints continue to limit CCUS scalability and competitiveness, reflecting the capital intensity of capture systems, the need for CO₂ transport storage and infrastructure, and broader regulatory and cost uncertainties. In many regions, carbon storage regulatory frameworks remain underdeveloped, with questions about permitting, liability, and public acceptance further slowing deployment.

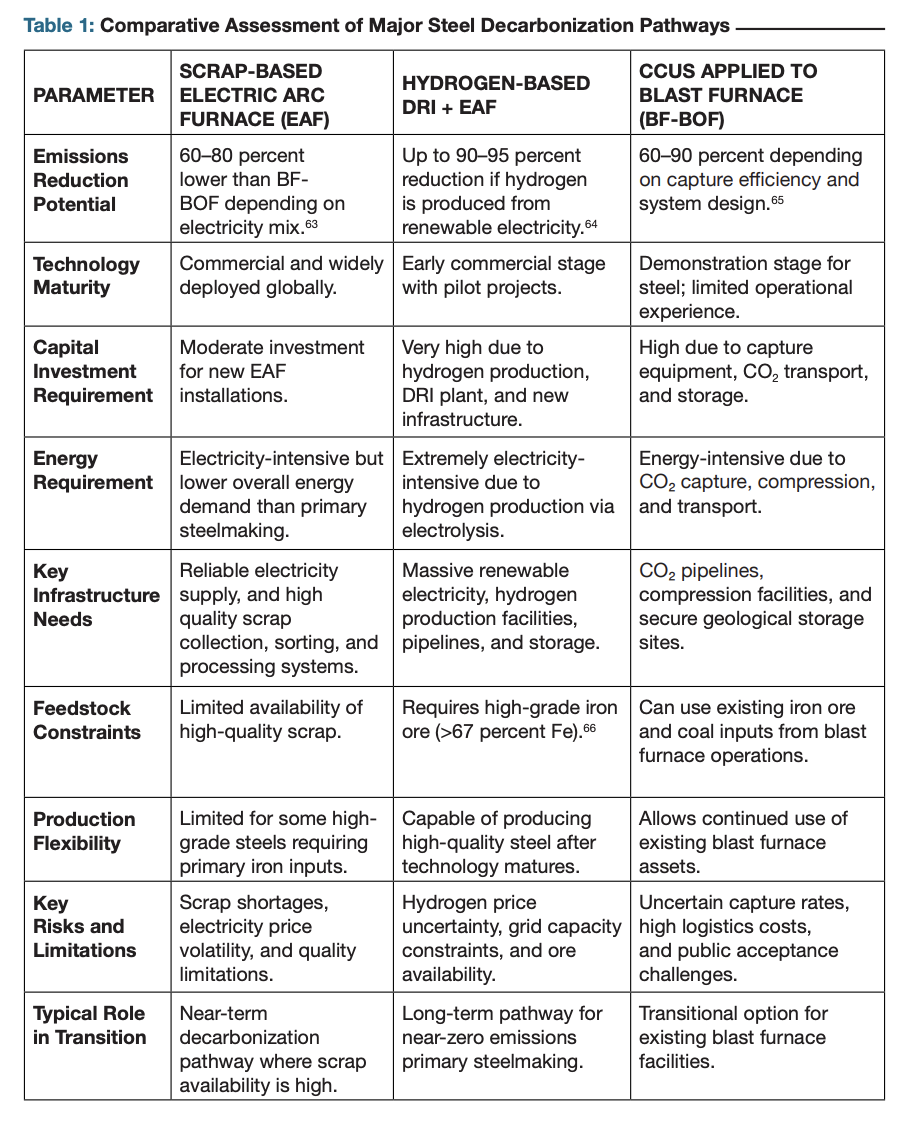

These developments illustrate that while technological pathways for green steel are emerging, scaling them will require far more than innovation at the plant level. As the comparison in Table 1 shows, no single pathway can deliver the full decarbonization of the steel sector on its own. Instead, the steel transition will likely involve a combination of technological approaches, deployed differently across regions depending on resource endowments, infrastructure readiness, and policy frameworks. In this context, the transformation of the steel sector will depend on the development of integrated energy systems, reliable supply chains for raw materials and hydrogen, and coordinated infrastructure investment across industries and regions.

V. THE FINANCE BOTTLENECK: MAKING GREEN STEEL BANKABLE

While much of the public debate around steel decarbonization focuses on technological readiness, one of the most significant barriers is increasingly financial and commercial. The challenge is not primarily a shortage of capital, as major steel companies and institutional investors have access to significant financing, but the absence of clear market signals and policy frameworks that justify large-scale investments in low-emissions production. In other words, the key constraint is the lack of a sufficiently credible business case to mobilize capital at scale.

Steel decarbonization would require a significant expansion of capital across both industrial assets and supporting infrastructure. Even without a technological shift, the global steel sector is expected to require about $47 billion annually over the next three decades to meet rising demand and maintain existing capacity. Transitioning to net-zero-compatible technologies could add another $8-$11 billion per year, or roughly $235-$335 billion by 2050, much of it directed toward renewable power, hydrogen production, and carbon transport and storage systems.

The economic barrier is commonly described as the "green premium," referring to the additional cost of producing lower-emissions steel, which may be reflected in higher prices for buyers depending on how costs are distributed across the value chain. This premium arises from several factors, including the capital intensity of new production assets such as hydrogen-based DRI plants, the cost of renewable electricity and green hydrogen, and the infrastructure required to support new industrial processes. Hydrogen prices remain a critical determinant of future competitiveness. Even in regions with abundant renewable resources, the capital investment required for electrolyzers, grid expansion, and industrial infrastructure can significantly raise project costs. For emerging economies, these challenges are further amplified by higher borrowing costs. Elevated weighted average cost of capital levels in markets such as India and Brazil can substantially increase the overall cost of hydrogen-based steelmaking, creating a major barrier to project bankability.

Financing challenges are also closely tied to policy alignment and demand creation. Without clear signals from governments and major industrial buyers, producers face substantial uncertainty regarding whether markets will reward lower-emissions steel. In this context, public procurement is emerging as an important mechanism for demand creation. Governments, as large infrastructure investors, have the ability to aggregate demand for green steel and provide long-term purchase certainty for producers. Some countries have already begun experimenting with such approaches. In Japan, for example, government procurement policies are beginning to favor lower-emissions materials in public infrastructure projects. However, institutional fragmentation often limits the effectiveness of these initiatives, as ministries responsible for infrastructure procurement may not have the fiscal resources to absorb the green premium without coordinated support from industrial policy agencies.

Beyond demand signals, innovative financial structures will be essential to bridge the early stages of the transition. Contracts for difference, long-term offtake agreements, and blended finance mechanisms are increasingly being explored as tools to reduce investment risk. Blended finance, combining concessional capital with private investment, can serve as a risk-absorbing layer for early demonstration projects. These first-of-a-kind projects play a critical role in establishing performance benchmarks, reducing perceived technology risks, and creating precedents for commercial financing.

However, transparency and credible transition plans from steel producers are increasingly viewed as essential for attracting investment. Institutional investors do not require absolute certainty regarding technological pathways, but they do require clarity regarding corporate strategies, policy engagement, and long-term emissions reduction trajectories. A persistent knowledge gap also remains within parts of the financial sector, where understanding of emerging steelmaking technologies such as hydrogen-based ironmaking remains limited. Improved dialogue between industry, policymakers, and financial institutions will therefore be necessary to build investor confidence.

Therefore, steel decarbonization is not constrained by the availability of capital alone. Rather, the core challenge lies in aligning policy frameworks, market demand, and financial instruments so that investments in low-emissions steel production become commercially viable. Until such alignment emerges, the deployment of green steel technologies will continue to progress more slowly than technological advances would otherwise allow.

VI. COORDINATING THE STEEL VALUE CHAIN: DATA, INFRASTRUCTURE, AND INSTITUTIONS

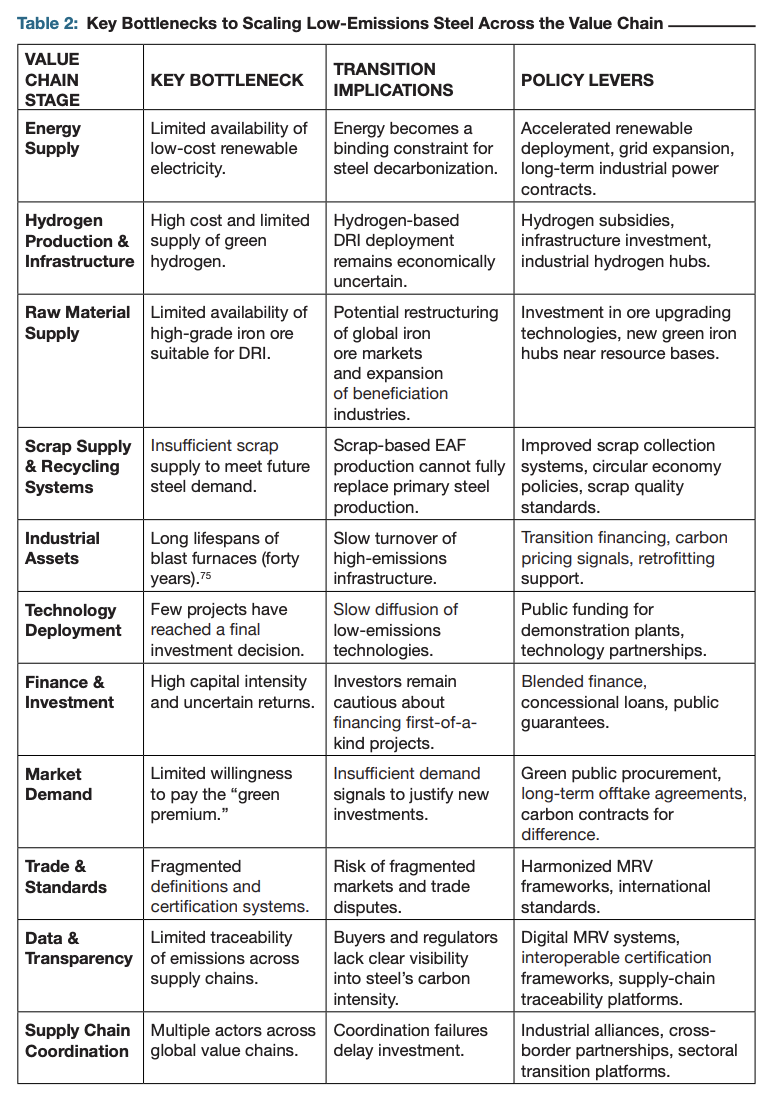

Beyond technology and finance, the transition to low-emissions steel ultimately depends on coordination across an increasingly complex global value chain. Steel production links mining, energy systems, industrial processing, manufacturing, and international trade. Decarbonization therefore requires new forms of collaboration across governments, producers, buyers, and regulators. Without such coordination, emerging green steel markets risk fragmentation, higher compliance costs, and slower deployment of low-emissions technologies. The transition to low-emissions steel faces multiple structural barriers across the value chain. Table 2 summarizes the major bottlenecks currently constraining the scale-up of green steel production, along with potential policy responses.

One critical dimension of this coordination challenge relates to the availability of reliable data and transparency across supply chains. Credible MRV systems are essential for green procurement programs, investor confidence, and cross-border trade in lower-emissions materials. Yet certification frameworks remain uneven across jurisdictions, and emissions information is often lost as steel moves through multiple suppliers, contractors, and intermediaries. Digital integration could help address this gap by linking certification systems with procurement platforms, potentially through application programming interfaces, to track environmental product data across supply chains. Strengthening chain-of-custody mechanisms that verify both the environmental performance of production facilities and the emissions intensity of specific steel products will therefore be critical in improving transparency and building trust in emerging green steel markets.

Beyond information transparency, physical infrastructure deployment also presents major coordination challenges. Large-scale industrial projects often require approvals across multiple regulatory authorities, including environmental agencies, energy regulators, land-use authorities, and local governments. Recent developments in Europe illustrate these constraints clearly. In 2024-2025, ArcelorMittal delayed final investment decisions on several green steel projects and canceled two major projects in Germany, while pausing others in Spain and France, citing high electricity costs, limited availability of affordable green hydrogen, and weak market conditions. Similarly, Thyssenkrupp placed plans for long-term hydrogen procurement on hold because of higher-than-expected prices. Hydrogen infrastructure, carbon transport networks, and renewable energy installations frequently fall under separate regulatory regimes, creating lengthy approval timelines and administrative complexity. Even in countries with strong industrial policy frameworks, permitting delays can extend project timelines by several years.

Infrastructure sequencing presents another critical challenge. Hydrogen-based steel production depends on the simultaneous availability of renewable electricity, hydrogen production facilities, transmission infrastructure, and industrial conversion technologies. Delays in any one of these components can slow the deployment of the entire system. In many regions, grid expansion, hydrogen transport networks, and industrial infrastructure planning are proceeding on different timelines, making it difficult for steel producers to commit to large-scale investment decisions.

Institutional coordination is therefore emerging as a key factor in determining which countries move fastest in deploying green steel. Governments increasingly need to align energy policy, industrial policy, and infrastructure planning, areas that have historically been managed by separate institutions. Countries able to streamline regulatory processes, coordinate infrastructure investment, and provide long-term policy clarity are likely to attract a larger share of early green steel investment.

Workforce and industrial capability represent another often overlooked dimension of the transition. Emerging steelmaking technologies require specialized engineering skills, operational expertise in hydrogen systems, and advanced digital monitoring capabilities. In several regions, shortages of skilled labor and technical expertise could slow industrial transformation. Expanding training programs, strengthening collaboration between industry and research institutions, and investing in workforce development will therefore be essential in supporting the deployment of low-emissions steel technologies.

VII. POLICY IMPLICATIONS: WHAT NEEDS TO HAPPEN

The transition of the steel sector is a complex, system-wide transformation that requires coordination across energy, industry, and trade systems. Progress will depend on the ability of government and industry to align policy frameworks, infrastructure development, and market incentives across regions. The following recommendations outline several priority areas for policymakers and industry leaders to accelerate the scale-up of low-emissions steel production.

First, policymakers must frame the steel transition as an industrial competitiveness strategy rather than solely a climate obligation. Steel remains a foundational sector for infrastructure, manufacturing, and national development, and the transition to low-emissions steel carries similar importance for future economic growth and competitiveness. The shift toward low-emissions production will reshape global supply chains and increasingly determine the geography of industrial competitiveness. Countries that can align energy systems, raw material supply, and industrial policy around green steel production will be better positioned to capture emerging value chains, while those that move slowly risk industrial displacement. In this context, the transition should be understood not only as a decarbonization challenge, but as a strategic opportunity linked to energy security, economic resilience, and job creation.

Second, energy and industrial planning must be integrated. The most binding constraint in the transition is not the availability of steelmaking technologies, but the availability of abundant, low-cost clean energy. Hydrogen-based ironmaking, EAFs, and other emerging pathways require massive increases in renewable electricity generation, grid capacity, and supporting infrastructure for hydrogen production and transport. Because the majority of emissions originate from ironmaking rather than downstream steel processing, policy frameworks should increasingly focus on decarbonizing iron production itself, including the development of green iron supply chains linking resource-rich regions with industrial manufacturing hubs. Industrial decarbonization strategies therefore need to be closely aligned with national energy planning. In some cases, improving the carbon intensity of national electricity grids may have a larger effect on steel emissions than individual corporate power purchase agreements. Developing integrated industrial hubs, where renewable energy, hydrogen production, and ironmaking or steelmaking are co-located, offers one promising approach to reducing infrastructure costs and improving project viability.

Third, governments must create stronger and more predictable market signals. Public procurement policies can play a particularly important role by providing early demand for lower-emissions steel in infrastructure and public construction projects. Because the incremental cost of green steel is relatively small in many downstream sectors, often less than 1 percent of the final cost of automobiles or buildings, targeting "lead markets" can help absorb early green premiums and stimulate investment. At the same time, financial instruments such as contracts for difference, concessional lending, and blended finance can help reduce early investment risks and enable first-of-a-kind projects. National policy targets and clear transition road maps are equally important in providing the long-term certainty needed to mobilize private capital.

Fourth, international coordination and supply-chain transparency will be essential. Diverging definitions, certification systems, and reporting methodologies risk fragmenting global steel markets and creating new trade barriers. Greater interoperability in MRV frameworks, potentially supported by digital traceability systems, can reduce compliance costs and strengthen trust across supply chains. Cooperation mechanisms such as bilateral agreements under Article 6 of the Paris Agreement and industrial partnerships between producing and consuming economies may also play a growing role in facilitating technology deployment and managing transition risks.

Fifth, the transition must also account for industrial structure and workforce realities. Small and medium-sized steel producers, which represent a large share of capacity in several emerging economies, require targeted support to adopt cleaner technologies and certification systems. Similarly, the transition will require new technical skills associated with hydrogen production, EAFs, and advanced industrial processes. Ensuring a just and inclusive transition for workers and communities linked to the coal-steel value chain will therefore be an essential component of long-term industrial policy.

In conclusion, the decarbonization of steel is one of the most complex industrial transitions underway. Unlike many other sectors, it requires coordinated action across miners, energy providers, steel producers, manufacturers, investors, and governments. Technology pathways are emerging, but deployment will depend on whether these actors can align policies, markets, infrastructure, and financial systems around a shared pathway for transformation. For major producing and consuming countries, this will require the development of comprehensive national action plans in close coordination with industry stakeholders, supported by targeted policy measures. At the same time, the global nature of the steel supply chains means that no country will achieve this transition alone. Effective progress will depend on international cooperation and coordination, with the government playing a central role in aligning domestic policies and cross-border frameworks. Without such coordination, progress will remain fragmented. With it, the steel sector can move from isolated demonstration projects to a large-scale transformation capable of supporting a net-zero global economy.

ACKNOWLEDGMENTS

The authors are grateful to the participants of the day-long international convening on green steel held in Seoul on February 25, 2026, for their valuable insights and contributions. They also extend their thanks to Medha Prasanna (ORF America) for her research and convening support and to Anna Song (Korea Engagement Lead) and Elliot Mari (Technical Expert for Materials, Industrial Transition Accelerator) at Mission Possible Partnership as well as Lauren Huleatt (Head of Impact at Transition Asia) for their thoughtful review and feedback. The authors also gratefully acknowledge the support of the Sequoia Climate Foundation.

Cover photo courtesy: istockuser CGShutter.

Note: Citations and references can be found in the PDF version of this paper available here.