Background Paper No. 38

BY JEFFREY D. BEAN AND DHRUVA JAISHANKAR

I. INTRODUCTION: THE CRITICAL MINERAL LANDSCAPE

Critical minerals have emerged as a priority for national policymakers. In an era of intricate global supply chains, mineral resources that are essential to the economy and at risk of supply disruptions represent a unique choke point in a country’s ability to produce energy generation, storage, and distribution systems; military equipment; and data storage, transmission, and computational hardware. Because critical minerals are vital inputs to virtually every technology that shapes modern life, they play an outsized role in the global economy and national security.

Critical minerals and rare earth elements are not necessarily inhibited by their availability, but because established links in their supply chains are subject to sharp geopolitical and economic constraints. Three primary steps must take place before critical minerals can become a high-purity refined commodity to be used in manufacturing: (1) discovery and exploration, (2) mining and extraction, (3) refining and midstream processing. A fourth area, e-waste (4) recycling, offers a crucial path to supplement the supply chain. Each stage is subject to a set of unique political and economic hurdles; linking them together presents a far more daunting challenge.

The global critical minerals shortfall has been looming for over a decade but has been difficult to address for at least three reasons. One, the demand for critical minerals continues to rise sharply. The International Energy Agency (IEA) projects demand for critical minerals to double from 2025 to 2030 and quadruple by 2040. Two, the mining and refining of critical minerals is highly concentrated: the top three refining nations of key energy minerals rose from around 82 percent in 2020 to 86 percent in 2024. Three, investments in mining and processing are particularly challenging on economic and environmental grounds. Even under perfect circumstances, projects take a long time to develop and have to withstand cyclical markets, and struggle to attract private equity. Most countries — particularly democratic societies with market economies — must also contend with high capital costs, long-term risk, workforce and skills shortfalls, and outdated regulations. Political will and large subsidies are consequently required to develop national capabilities in discovery and exploration, mining and extraction, refining and processing, and recycling, even as private investment is key to long-term success.

Furthermore, critical minerals have proved central to ongoing geopolitical competition between the United States and its partners and allies on the one hand and China on the other. China refines and processes over 60-70 percent of cobalt and lithium globally, along with more than 90 percent of rare earth elements, which are critical to the production of batteries and permanent magnets. It holds a dominant position in the mining or refining and processing of many other strategic elements as well. And China has repeatedly demonstrated a willingness to use monopolistic market distortions to influence pricing and weaponize supply chains via export controls and bans, in some cases in exchange for technology transfers, market access, or other advantages.

The United States, meanwhile, is over 75 percent import dependent on twelve critical minerals in addition to rare earth elements. Countries like India are over 90 percent import dependent across the thirty minerals the country identified as critical in 2023. Even countries such as Australia and Canada, among the most mineral wealthy nations, face mid-stream processing constraints or limitations on specific minerals. For national security, energy security, and sustainability, and for basic growth and prosperity in an era of digital economies, cooperation in diversifying and strengthening critical mineral supply chains will be necessary.

Numerous countries have developed critical minerals lists. These lists greatly overlap but are rarely identical because vulnerabilities and demand are unique to each country’s geology, capacity, and requirements. The United States 2025 List of Critical Minerals, developed by the U.S. Geological Survey, includes sixty minerals, up from fifty in 2022. Unlike many other countries, the United States does not group heavy and light rare earth elements (REEs) or Platinum Group metals, resulting in larger lists. By contrast, the European Commission listed thirty-four critical raw materials in 2024, India’s Ministry of Mines identified thirty critical minerals in its 2023 study, Japan’s Ministry of Economy, Trade and Industry deems thirty-five minerals as critical, and South Korea’s Ministry of Trade, Industry and Energy names thirty-three critical minerals. Among resource-rich developed economies, Natural Resources Canada identified thirty-four critical minerals in an updated list, while the Australian government identified twenty-six critical minerals in its 2022 strategy.

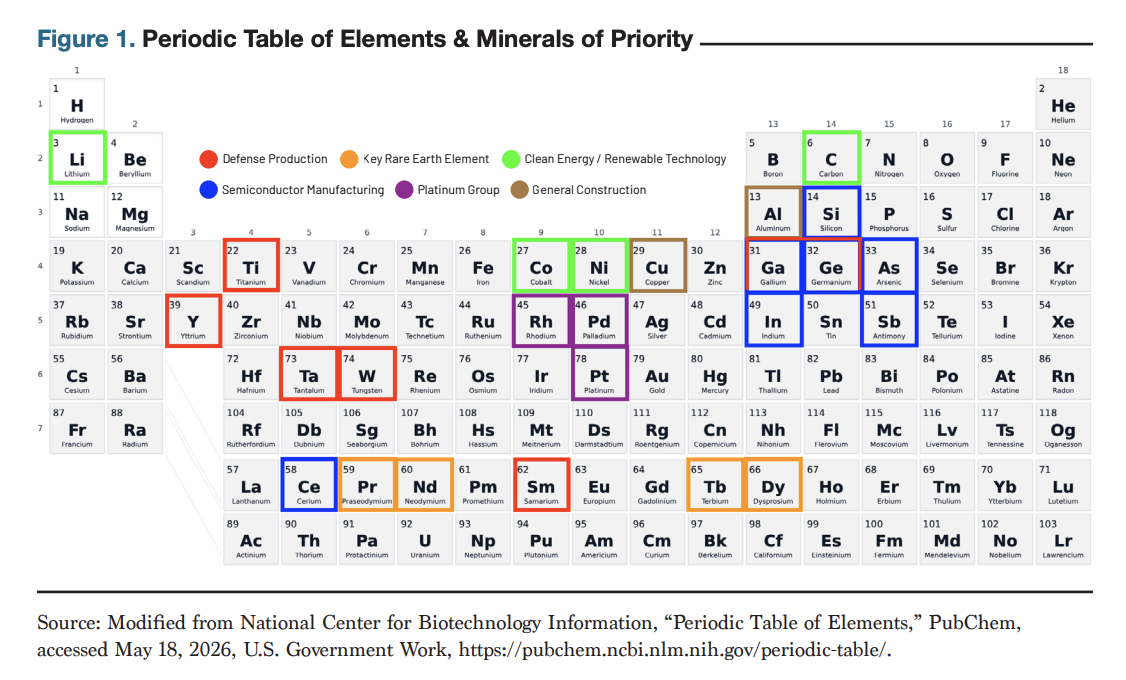

Overall, lithium, cobalt, nickel, and graphite—required for batteries—are near universally recognized as critical minerals, along with key rare earth elements (neodymium, praseodymium, dysprosium, and terbium) for magnets; gallium, germanium, silicon, arsenic, and cerium to produce semiconductors; and platinum group metals (platinum, palladium, and rhodium) used in catalysts. In addition, copper and aluminum, although widely available, are generally considered important for a variety of industrial functions, while titanium, tungsten, tantalum, yttrium, antimony, and samarium are vital for defense and dual use purposes. This paper assesses growing demands for these minerals — minus the platinum group — and the risk of disruption, as well as the prospects for international collaboration to address the shortfall among the United States, European Union, India, Japan, South Korea, Canada, and Australia.

II. ENERGY: BATTERIES, PERMANENT MAGNETS, AND WIND TURBINES

As the world grapples with ways to provide secure and sustainable energy, critical minerals prove themselves indispensable for batteries, solar cells, wind turbines, nuclear power plants, transmission hubs, and power cables, as well as their components. Copper is necessary for transmission; lithium, nickel, cobalt, and graphite for battery storage; and dysprosium for permanent magnets, meaning these elements are necessary for electric vehicles (EVs), smart storage, and wind turbines. Yet the majority of processing for all these minerals is dependent on Chinese sources.

Copper represents a prime example of a widely available mineral that confronts upstream challenges, including an estimated 30 percent shortfall by 2035. Growing electricity, data, and solar energy requirements through 2030 will place intense demand on copper for electricity transmission, thermal solutions for cooling electronics in data centers, photovoltaic cells, and batteries. Around 375,000 tons will be required annually by 2030 for new data centers alone. Declining ore grade, higher capital costs, and exhausted mines coupled with a lack of recent copper discovery will make recycling and exploration indispensable. Although 249 substantial copper deposits were discovered between 1990 and 2024, only a handful have been discovered since 2015.

With copper mines facing nearly two-decade lead times from discovery to extraction and with total demand by some estimates reaching over 50 million metric tons a year by 2050, this places significant burden on other portions of the chain (e.g., recycling and efficient deployment) to use copper more efficiently. For context, according to the U.S. Geological Survey, recycled copper totaled 850,000 tons in 2023, which accounted for 30 percent of U.S. copper supply that year. The existing sources of copper supply are less at risk from competitor inference in mining with Chile leading the way, and noteworthy output from Peru and Mexico, in collectively contributing to 37 percent of the world’s copper production. While China holds around half of the world’s copper smelting capacity (and most of its smelters are state-owned enterprises), many other states also have smelting capacity, including the United States, Chile, Europe, Democratic Republic of the Congo, Japan, South Korea, and India.

Aluminum is similarly used in a wide variety of industrial functions, including transportation, electronics, and construction. Derived from bauxite, whose deposits are widely found in Australia, Guinea, and Brazil, aluminum production is once again concentrated in China. India, Canada, and Australia, while among the top ten producers, combine for less than 20 percent of China’s production capacity. Scaling up aluminum production using cleaner and less carbon-intensive technologies will remain a challenge, one that will require cooperation among partners in heavy industrial decarbonization.

The global demand for lithium is expected to quintuple while nickel and graphite are also expected to double between 2030 and 2040, particularly for batteries, with these minerals already experiencing annual demand of 6-8 percent according to the IEA. Indonesia, Australia, and Brazil have significant nickel reserves, with possible finds in Canadian sulfide deposits and in Tanzania. Indonesia is the world’s leading nickel miner,

producing over 50 percent of global supply through laterite ore mining, whereas Canada and Norway represent notable players in nickel refining through firms Glencore, Sherritt International, and Vale. In recent years, Indonesia has had some success in increasing its domestic processing capacity, offering useful lessons to others, but outright bans on exports as Jakarta undertook would be unhelpful. Graphite reserves in Brazil and Madagascar, as well as the further exploitation of deposits in Mozambique, offer upstream possibilities. Lithium deposits in Chile and Argentina are vital, with the United States, Canada, and Australia also offering possibilities.

Meanwhile, cobalt and rare earth elements dysprosium and neodymium are requisite to permanent magnets, such as those used in electric vehicle motors and wind turbines. Demand for these elements is expected to grow by 50-150 percent in the next decade. Cobalt reserves are concentrated in the Democratic Republic of the Congo but also exist in Morocco, Australia, and Indonesia. Dysprosium can be found in Myanmar and Australia, with neodymium present in Vietnam, Brazil, Australia, and the United States. Terbium, also used in magnets in EVs and wind turbines, is concentrated in China, with Japan discovering deposits in deep sea mud in 2018.

III. DEFENSE: STEALTH FIGHTERS, NIGHT VISION, AND LASERS

In defense applications, critical minerals and rare earth elements play a fundamental role in the systems that military leaders use. These include C4ISR (Command, Control, Communications, Computers, Intelligence, Surveillance, and Reconnaissance) capabilities that shape threat assessments and planning as well as the operational capabilities that militaries use on the battlefield. For example, radio sets require lithium-ion batteries, night vision goggles utilize antimony, thermal imagining systems require germanium, and range-finding capabilities require yttrium and neodymium.

Currently, titanium, tungsten, and tantalum matter play important varied roles in many military applications; antimony and germanium have multiple uses in defense equipment but are severely supply constrained; the rare earth yttrium’s properties make it essential for lasers, range finders, and precision weapons systems; while samarium is used in guidance systems and represents a point of high vulnerability. Fifth-generation fighter airframes require titanium alloys, while their jet engines use rare earth magnets and tungsten turbine blades and components coated in tantalum for heat resistance. Crucial military aircraft components require germanium, gallium, samarium, praseodymium, and antimony, including for precision guidance and armor-piercing weaponry. As these examples illustrate, critical minerals and rare earths are foundational to the specialized systems used in defense operations.

Titanium will witness a steady demand growth with early exploration and recovery potential identified in Australia, India, Saudi Arabia, and mineral sands in Mozambique and Madagascar. Vietnam boasts tungsten reserves, with South Korea reopening a mine in Sangdong and the United Kingdom attempting to reopen a facility in Hemerdon. Tantalum is concentrated in central Africa (particularly the Democratic Republic of the Congo and Rwanda) and in Australia. Tajikistan, Turkey, the United States, and Australia have antimony deposits, while germanium may be extracted as a by-product of coal ash and zinc refining in countries like Canada and the United States. Gallium too is a by-product of bauxite and zinc processing, with the United States, Canada, European Union, and Australia examining recovery project and by-product extraction for its use in semiconductors and EVs.

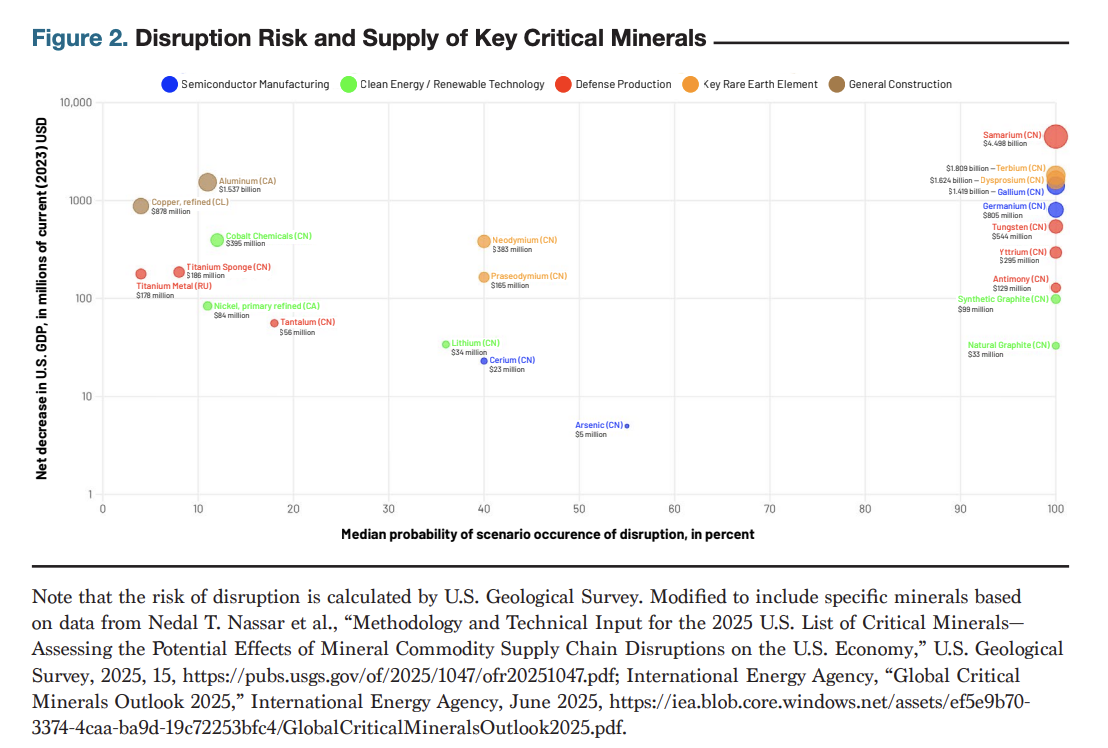

Among rare earth elements, yttrium — crucial for lasers — can be found in Australia, Brazil, and Africa, with possible ionic clay deposits in Southeast Asia. China produces 99 percent of the world’s supply of samarium, a heavy rare earth, which is irreplaceable in guidance for missiles and space applications. Its disruption risks a net loss to the gross domestic product of $4.5 billion for the United States. Samarium deposits — along with praseodymium — have been explored in Australia, the United States, Tanzania, and Malawi.

IV. SEMICONDUCTORS & HIGH TECHNOLOGY MANUFACTURING

In high technology manufacturing, the semiconductor industry is representative of the need and uses for strategic elements. The industry’s core manufacturing phrase includes both the front-end process of fabrication on a high purity wafer, through deposition, photo-resist coating, lithography, etching and cleaning, and ion implantation, and the backend process of assembly, marking, testing, and packaging to prepare the chip for attachment to a broader circuit board. Supplies of minerals like gallium, germanium, silicon, and the rare earths cerium and neodymium are all pivotal in different aspects of production or finished products.

Gallium, produced as a by-product of zinc and aluminum mining, serves as a linchpin for modern semiconductors — including compound semiconductors utilized in commercial products and advanced defense systems. When combined with oxygen, nitrogen, or arsenic, gallium forms semiconductor material that exceeds the performance of the most commonly used mineral, silicon, because of a wider band gap. Gallium nitride is used in advanced microelectronics, satellites, radio communication devices, LiDAR, and white LEDs and can power on and off more quickly and operate more efficiently. Semiconductor wafers made with gallium arsenide can also operate at higher frequencies and are more heat-resistant than those made with silicon.

The United States has a 100 percent import dependency for finished gallium products but sources it from a diverse base, including Japan, China, and Germany. Despite China’s significant production (it controls 98 percent of low purity production as of 2024), the diverse supplier base somewhat mitigates potential risks. Yet China still holds the keys on the essential processing plants. Japan, Germany, and Australia are attempting to produce primary gallium. Silicon — while widely available in the Earth’s crust — similarly sees its production concentrated in China, which accounts for about 80 percent of global production. Silicon has important uses in solar photovoltaics, semiconductors, and transistors. Its advantages of lying halfway between a conductor and insulator enable manufactures to create high precision electron flows via the transistors used in microchips. U.S. firm Hemlock Semiconductor is the sole large hyper purity polysilicon manufacturing plant in the United States, producing 30,000 – 35,000 tons annually. Chinese firms account for 93 percent of global polysilicon production. Improving production in Brazil, Europe, India, and Canada, among other places, would increase global resilience. In recent years, investments in polysilicon production in the Gulf – particularly Saudi Arabia and Oman – offer examples of diversification.

Within chips, copper is still widely leveraged for interconnects, with cobalt sheathes and caps to protect against electromigration at the atomic scale. Cobalt has wide industrial uses but does not occur in nature on its own and is usually found with copper and nickel deposits. Supplies of germanium, like silicon and gallium, are important because there is a lack of substitutes at scale for these three foundational minerals in chip production. Similar to gallium, germanium wafers offer different properties when used in chips, including higher frequencies and greater power efficiencies. The element also has unique benefits as a direct band element to manipulate light and thus is used as an irreplaceable dopant in fiber optics. Its role in fiber optics for GPU-heavy AI data centers is notable because server racks used in these cutting-edge hyperscalers use five times more fiber optic cable than a traditional server rack. In 2024, 44 percent of germanium consumption by revenue was for fiber optics. In 2025, around $66 million worth of refined germanium was imported to the United States, with China, Russia, and the United States the leading miners globally. Additional producers to offset China’s grip on production for germanium metal and germanium dioxide (it had 60 percent of global processing as 2025), include Canada, Belgium, and expanded U.S. sources. Due to the aforementioned mining and processing supply chain constraints driven by Chinese export controls, germanium is also a prime candidate for e-waste recycling, with 30 percent of consumed germanium recovered annually from recycled electronic devices as of 2020 as well as from decommissioned tanks and armored vehicles.

Cerium is indicative of several rare earths used in different aspects of chip manufacturing. Cerium oxide slurries are used during fabrication processes immediately before lithography to finish and clean wafers through chemical-mechanical planarization. In plain terms, they polish and flatten the wafers both to help ensure deconfliction between active areas and insulators and create a pristine surface for microscopic lithographic pattern projection. Cerium is widely abundant in nature and accrued during bastnäsite and monazite mining and used in other applications like catalytic converters. Today, China still holds a majority of the world’s extraction efforts and processing capacity of cerium, although the United States, Australia, and Malaysia also play roles in the upstream supply chain, and there are many consumers downstream. As a result, and because of stable market prices, it is viewed as a commodity at moderate to low risk of disruption.

Rare earth magnets, built around neodymium, play an essential function in semiconductor manufacturing equipment. Specifically, sintered neodymium iron boron (NdFeB) magnets have a pivotal role in advanced chip manufacturing. NdFeB magnets are utilized in ASML’s extreme ultraviolet lithography machines to reduce vibrations and minimize friction during photolithography. They are also used in chemical vapor deposition, etching, and pump tools and equipment.

V. MULTILATERAL AND MINILATERAL INITIATIVES

De-risking critical mineral supply chains will require cooperation among a variety of actors, including U.S. allies and partners and between the developed and developing worlds. Following the completion of the Section 232 investigation on critical minerals in October 2025, U.S. president Donald Trump directed the U.S. government to continue the process of addressing the critical minerals deficit with international partners through various authorities, tools, and relationships, including new partnerships. These partnerships include three main U.S. government-led efforts: Pax Silica, the Forum on Resource Geostrategic Engagement (FORGE), and Project Vault. In addition, critical mineral coordination is underway among the Group of Seven Plus and Quad (Australia, India, Japan, and the United States) groupings. The United States in early 2026 hosted two ministerial sessions involving many of the same partners to coordinate strategies and commit to pricing and offtake arrangements. There are also non-U.S. minilateral efforts, such as that involving Australia, Canada, and India (ACITI), in addition to various bilateral and public-private initiatives. Moreover, cooperation with and investment in major mineral-producing countries in the Global South—Chile, Peru, Mexico, Argentina, and Brazil in Latin America; Indonesia, Myanmar, and Vietnam in Southeast Asia; and the Democratic Republic of the Congo, Rwanda, Mozambique, Madagascar, Tanzania, Zambia, and Zimbabwe in Africa — will be crucial.

Three prominent U.S.-led efforts under the Trump administration involve multiple countries. Pax Silica is a U.S.-led group of fifteen signatory nations and growing (including Australia, Finland, Greece, India, Israel, Japan, Norway, the Philippines, Qatar, South Korea, Singapore, the United Arab Emirates, the United Kingdom, and Sweden) launched in December 2025 and led by the U.S. State Department to support projects to secure the key facets of the critical and emerging technology supply chain. Pax Silica’s first tangible initiative, a fund inaugurated in March 2026 with a U.S. commitment of $250 million and goal to raise $1 trillion, intends to support various projects across the AI value chain. How that fund will address critical minerals remains to be seen.

A second effort involves the FORGE. On February 4, 2026, during the U.S.-hosted Critical Minerals Ministerial, Secretary of State Marco Rubio announced the launch of a new initiative that builds on the preceding Minerals Security Partnership (MSP). For context, the MSP launched under the Biden administration in 2022, involved fourteen members: Australia, Canada, Estonia, Finland, France, Germany, India, Italy, Japan, Norway, South Korea, Sweden, the United Kingdom, the United States, and the European Union. Whereas the MSP had a high focus on environmental sustainability, FORGE appears to be more results orientated and will potentially serve as a mechanism for price protections (notably price floors) to mitigate coercive impacts from China. South Korea, who was MSP chair for this period, will chair FORGE through June 2026. Such a customs union to insulate against Chinese coercion by setting price floors would likely be most useful for minerals not traded on the London Metal Exchange or those subject to high volatility. Securing supply of cobalt, for example, may require price floors, although other policy measures would be required to ensure such price floors work effectively without unnecessary inflationary or distortionary impacts. Furthermore, not every mineral (especially bulk minerals) will benefit from that form of intervention.

Thirdly, Project Vault represents a new U.S. effort to stockpile critical minerals for domestic commercial use led by the Export-Import Bank of the United States (EXIM). Announced on February 2, 2026, by EXIM chair John Jovanovic, the project aims to establish a U.S. Strategic Critical Mineral Reserve, an “independently governed public-private partnership that will store essential raw materials in secure facilities across the United States.” The effort is supported by $12 billion in commitments: a $10 billion loan from EXIM Bank over fifteen years and $2 billion in commitments from the private sector. Which minerals it covers and how and under what circumstances firms will ultimately apply for withdrawals is still to be confirmed.

Similar stockpiling initiatives have been discussed in partner countries including South Korea, India, and the European Union, or in Japan’s case expanding existing initiatives, with the difference that many of these initiatives cover both commercial and defense use, whereas the United States has maintained a long-standing separate stockpile for defense materials (National Defense Stockpile) for which strategic and critical materials are managed by the Defense Logistics Agency. Stockpiling represents only a temporary band-aid for a crisis, especially for high-volume minerals.

Critical minerals are also increasingly making their way into existing multilateral cooperative frameworks, such as the G7 and the Quad. In July 2025, the G7 leaders in Kananaskis, Canada, agreed to advance a multiyear effort to sign a formal action plan, which intends to build standards-based markets, mobilize capital and responsible mutual investments, and promote innovation in processing, intellectual property licensing, and recycling. This translated into a Critical Minerals Production Alliance, meant to link the G7’s action plan and road map with commitments to specific projects. U.S. treasury secretary Scott Bessent hosted a follow-up meeting on January 12, 2026, which featured finance ministers from the G7, along with ministers from Australia, India, Mexico, South Korea, and the EU — all of whom have endorsed the plan. The meeting focused mostly on information sharing related to Chinese coercive practices in the critical minerals supply chain and the need to build decoupled resilient alternatives.

Meanwhile, the Quad has a critical mineral working group. In July 2025, the grouping also announced a critical mineral initiative following the Quad foreign ministers meeting in Washington. While there are logical roles for each partner among the Quad countries, and supply chain monitoring and information sharing has been a focal point for several years, specific initiatives announced in May 2026 under this banner include e-waste recycling and minerals recovery and reprocessing among the twenty designated critical minerals that the partners have in common.

Another promising initiative that does not involve the United States is the Australia-Canada-India Technology and Innovation ACITI Partnership. Announced via joint statement in November 2025, the arrangement includes a focus on supply chain cooperation and explicitly mentions critical minerals. Each of the partners currently has existing memoranda of understanding (MoUs) on a bilateral basis with one another tied to trade, supply chains, and critical minerals. With deep experience and private sector heft from Canada and Australia, including giants like Rio Tinto and Barrick, and some nascent opportunities to develop refining and processing in India, the agreement has real potential to support supply chain coordination for specific critical minerals in renewable energy applications and products. Australia has large reserves of lithium, cobalt, tantalum, rare earth elements, and uranium and, along with Canada, has deep mining expertise and an attractive investment and regulatory environment. Canada is a producer of aluminum, cobalt, indium, platinum, and palladium. India brings lower-cost manufacturing and demand, meaning complementarities.

Other bilateral initiatives, such as between the United States and India, or the United Kingdom and India, can complement such efforts. The European Union has also been playing an active role. In addition to a U.S.-EU Action Plan for Critical Minerals Supply Chain Resilience, the EU has been actively partnering with countries such as Angola, Namibia, and South Africa, including in the Lobito Corridor, clean energy investments in Namibia, and new kinds of investment partnerships with Angola and South Africa.

In addition to cooperation with developed economies, India can play an important role in working with mineral-rich countries in the developing world, particularly Africa and to a lesser extent Latin America. In Zambia, the co-owned Indo-Zambia Bank can finance mineral cooperation. Zambia is particularly rich in copper and cobalt and has nickel deposits. Zimbabwe, similarly, has potential for lithium extraction. Within the erstwhile MSP, Indian entities had indicated interest in co-investing in mineral projects in Latin America. For example, in February 2026, India and Brazil entered into a framework agreement on critical minerals, and Indian state-owned mining conglomerate KABIL has begun exploration of five lithium blocks in northwestern Argentina in a $24 billion mining project. More such efforts that engage key mineral-rich countries in the Global South would help to create downstream, midstream, and upstream alternatives to China’s stranglehold on critical mineral supply chains.

VI. CONCLUSION AND RECOMMENDATIONS

While a host of bilateral MoUs have been signed by the United States and its partners on critical minerals, attempts at true multilateral or minilateral cooperation are nascent, while public-private efforts remain challenging. Two areas for further research and investigation present themselves. First, how can the United States and its partners and allies effectively coordinate new initiatives and industrial policies tied to critical minerals in the midst of a scramble for self-sufficiency to avoid self-defeating competition? Second, what are the implications for the future global trading order if greater levels of customs union-style coordination are sought to redress imbalances in critical materials through price floors?

First, at the exploration stage, enhancing the resolution of data for national geological surveys and ensuring that data and information gathered for claims is cumulative would create further opportunities. Conducive tax and regulatory environments for miners and market opportunities to sell the rights to claims could also benefit from closer inter-governmental coordination. It is notable that U.S. investments in exploration have actually declined, despite growing demand. The G7 and key partners, such as Australia, India, Mexico, and South Korea, could coordinate information sharing and alignment for exploration efforts.

Second, on mining and extraction, joint investments using state-backed investors and sovereign wealth funds will be required in key resource-rich countries. In the United States, the U.S. International Development Finance Corporation could lead such efforts, in conjunction with analogous institutions in Japan, South Korea, and India, as well as private investors such as Mubadala and Temasek, with Pax Silica being a useful steering mechanism for investing in such efforts. A handful of countries in Africa (DRC, Zambia, and Mozambique), Southeast Asia (Indonesia and Vietnam), and Latin America (Chile, Bolivia, and Argentina) could be the focus of long-term commitments to mining and extraction.

Third, to incentive large-scale investment in mid-stream processing, off-take agreements will need to be aligned. FORGE represents the most promising medium by which to do so. This would involve offtake for both mined and extracted ore as well as for refined and processed ore, including through government procurement initiatives. In addition, efforts such as ACITI—coalitions of mineral-rich countries and those with lower-cost processing and demand—could complement such efforts.

Finally, on recycling, building on efforts at the Quad critical mineral working group would be most practical, bringing in other partners with technical capabilities and recycling potential, while jump-starting efforts like the U.S.-India Strategic Mineral Recovery initiative to serve as a proof of concept. The announcement on May 26, 2026, at the Quad Foreign Minister’s meeting of the initiative to mobilize $20 billion for the Quad Critical Minerals Initiative Framework provides the policy basis to promote deeper e-waste and scrap recycling among these four partners.

ACKNOWLEDGMENTS

The views and analyses expressed herein are those of the authors and do not necessarily reflect the position of ORF America, its affiliates, or partner institutions. The authors are grateful to Erika Ingvald and Karthik Bansal for their reviews and thoughtful comments on an earlier draft of this paper, and to Arthur Hur for edits. Any errors that may remain are those of the authors’ alone.

Cover image courtesy user istock80.

Note: Citations and references can be found in the PDF version of this paper available here.