Special report no. 11

BY PIYUSH VERMA, MEDHA PRASANNA, AND SARAH SALAH

I. INTRODUCTION

As the European Union (EU) accelerates its Green Deal agenda and increasingly projects its climate ambitions through trade, investment, and industrial policy, its engagement with the Global South is entering a decisive phase. Instruments such as the Carbon Border Adjustment Mechanism (CBAM), the Global Gateway, and the emerging framework of Clean Trade and Investment Partnerships (CTIPs) reflect Brussels’ effort to align economic cooperation, industrial competitiveness, and climate objectives in a rapidly changing global economy.

Yet beyond political momentum and policy rhetoric, CTIPs remain conceptually fluid and operationally underdeveloped. For developing economies across Asia, Africa, and Latin America, critical questions remain. What does a “partnership” mean in practice? Can CTIPs support green industrialization, technology cooperation, local value creation, and climate finance mobilization, rather than introduce new trade barriers and compliance burdens? And how can the EU ensure that CTIPs are genuinely mutually beneficial — strengthening global resilience and sustainable industrial development while also advancing Europe’s own strategic and economic interests?

This report draws on ORF America’s broader work on clean industrial transitions, trade, and North–South cooperation, and in particular on the EU–Global South Dialogue on Clean Trade and Investment Partnerships convened by ORF America in Brussels in April 2026. While the analysis focuses primarily on EU‑level frameworks, it recognizes that the effectiveness of CTIPs will also depend on how individual EU member states engage, invest, and coordinate with partner countries. Against this backdrop, the report critically examines the evolving architecture of CTIPs and proposes practical pathways for making them more credible, implementation-oriented, and genuinely co-created with the Global South.

II. EVOLUTION OF EU’S GREEN TRADE DIPLOMACY

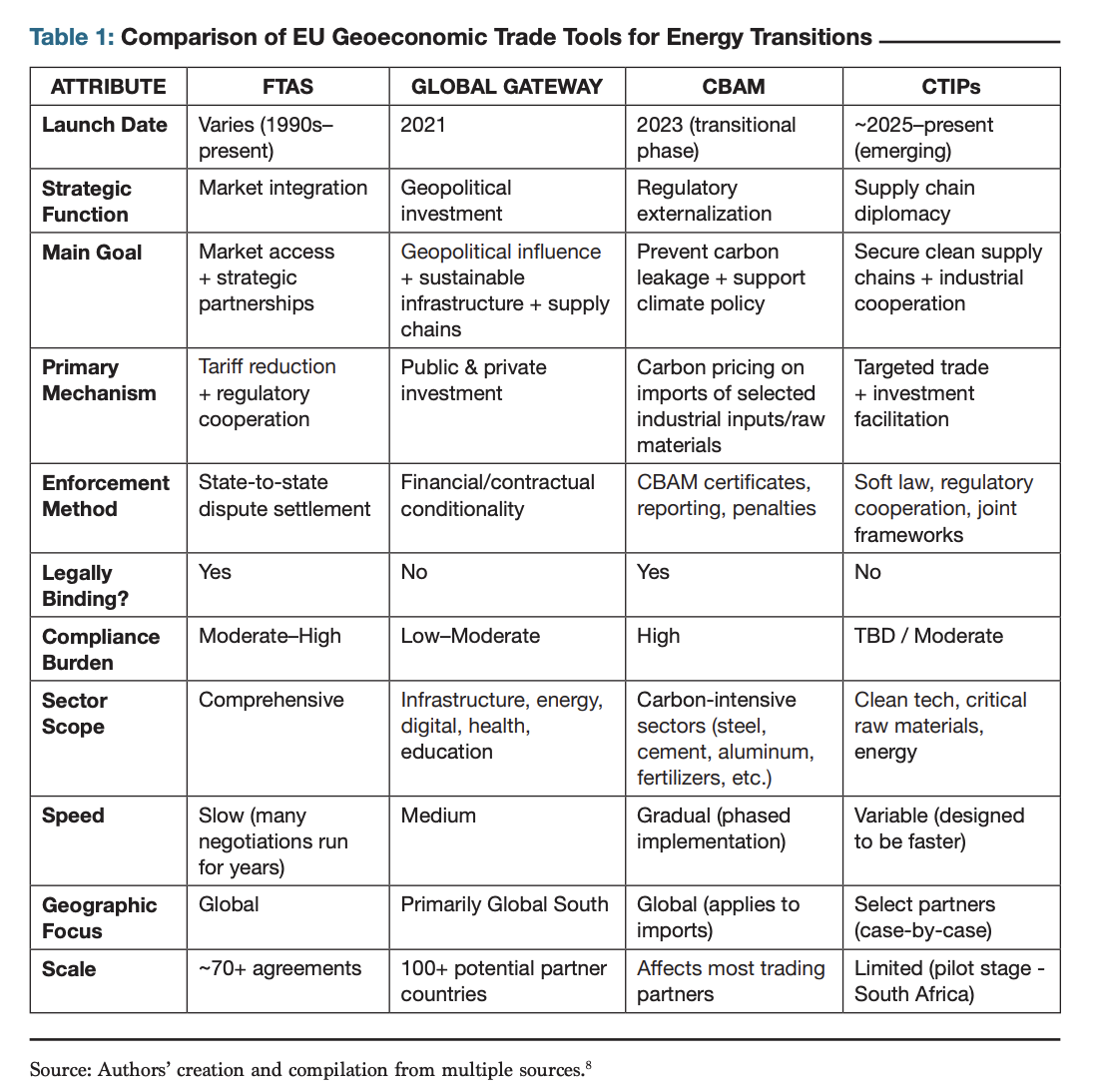

The emergence of Clean Trade and Investment Partnerships (CTIPs) cannot be understood in isolation, but rather as part of a broader shift in the EU’s external economic strategy that increasingly integrates trade, climate, industrial policy, and geopolitics. Instruments such as the CBAM and Global Gateway reflect the EU’s growing effort to align external economic relations with climate and industrial objectives. Historically, European countries have relied largely on two primary tools: free trade agreements (FTAs) to expand market access and Official Development Assistance (ODA) to support development cooperation and project soft power. However, these instruments often lack the speed, flexibility, and integrated industrial approach required for the energy transition era.

At the same time, energy and clean technology supply chains have become deeply intertwined with economic security, military readiness, and geopolitical competition. The concentration in China of critical raw materials (CRMs), downstream mineral processing, and clean technology manufacturing, coupled with heightened concerns over supply chain disruptions following the COVID-19 pandemic, Russia’s invasion of Ukraine, and the conflict surrounding the Strait of Hormuz, has accelerated EU efforts to reduce strategic dependencies and strengthen resilient partnerships. These vulnerabilities have implications not only for partner countries but also for Europe itself. Persistent uncertainty over the availability and affordability of energy and critical raw materials, underscored most visibly by disruptions to European gas supplies, has affected the speed, scale, and cost of the EU’s own energy transition and reshaped the political economy of energy within and beyond its borders, sharpening the geopolitical stakes of how Brussels manages its external partnerships. In this context, the EU’s contemporary geoeconomic strategy increasingly seeks to reshape globalization through a climate and competitiveness lens while reinforcing industrial resilience and geopolitical influence. Since 2019, a growing number of outward-facing EU initiatives have been anchored in this broader strategic objective. Yet it remains unclear whether the EU’s expanding suite of green trade instruments will ultimately foster genuinely mutually beneficial partnerships or further complicate the energy transition pathways of developing economies.

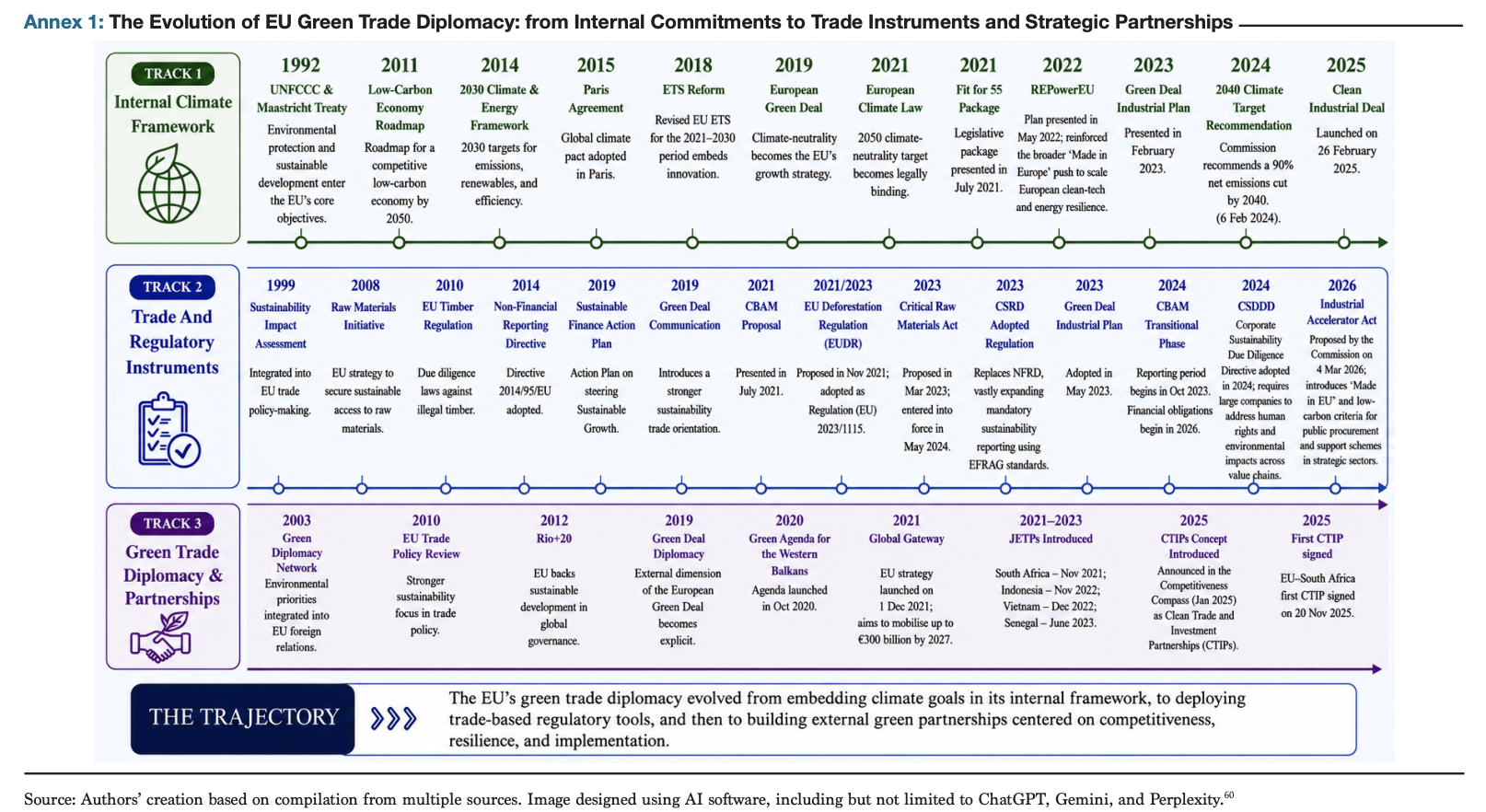

The foundations of the European Green Deal and the EU's broader environmental governance framework can be traced back to the 1990s, particularly the Maastricht Treaty and the signing of the UNFCCC, which embedded environmental protection and sustainable development within the EU's policy architecture (see Annex 1). It codified key principles like the Polluter Pays Principle (PPP) into EU law. Over time, environmental considerations became increasingly integrated into EU trade and foreign policy. Since 1999, Sustainability Impact Assessments and since 2011 Trade and Sustainable Development (TSD) chapters have accompanied EU trade negotiations to evaluate the environmental, social, and economic implications of proposed agreements. The establishment of the Green Diplomacy Network in 2003 further institutionalized climate and environmental priorities within EU external relations.

The 2019 European Green Deal marked a major turning point by transforming earlier climate ambitions into a comprehensive economic and industrial strategy aimed at achieving climate neutrality by 2050, a target later codified under the European Climate Law in 2021. Since then, the EU has increasingly leveraged trade and investment instruments, including CBAM, Global Gateway, and now CTIPs, to externalize elements of its climate and industrial agenda while attempting to mitigate competitiveness risks associated with its domestic decarbonization policies (Table 1). These steps have reinforced the EU's self-image as a climate frontrunner. Yet many developing economies view the bloc as a partner whose multilateral climate diplomacy has often outpaced the delivery

of finance, technology, and equity on the ground. From this perspective, the external dimension of the Green Deal can be read as an effort to convert that posture into more tangible and mutually beneficial partnerships.

The Industrial Accelerator Act (IAA), presented by the European Commission in March 2026, marks a further evolution in this trajectory. Unlike CBAM, which operates primarily as a regulatory instrument, or Global Gateway, which functions as an investment-mobilization framework, the IAA is designed to create demand for low-carbon and strategically resilient industrial production inside the EU through public procurement, public support schemes, low-carbon product differentiation, permitting acceleration, and “Made in EU” provisions. Its focus on steel, cement, aluminum, automotive components, net-zero technologies, and critical raw materials underscores the extent to which climate policy, industrial competitiveness, and supply-chain security are now being integrated within EU domestic economic policy. However, the IAA also exposes a gap in the EU’s external clean industrial strategy. CTIPs are framed as partnership mechanisms for clean value-chain cooperation with selected non-EU countries, but the current IAA framework does not provide a clear role for CTIP partners. This creates a potential disconnect between the EU’s external partnership rhetoric and the demand-side instruments that will shape actual investment flows, procurement opportunities, and market access.

CBAM represents the clearest example of this shift. Designed to equalize the carbon cost of imports with the carbon price faced by EU producers, CBAM seeks to prevent carbon leakage and protect the competitiveness of European industry as climate regulations tighten domestically. In practice, it also signals the EU's ambition to shape global standards around carbon-intensive production and supply chains. For many developing economies, however, instruments such as CBAM are experienced primarily as an additional cost embedded in their production processes, and are increasingly read as a means of ring-fencing EU industry by shifting competition toward carbon and sustainability standards on which European producers hold an advantage." Countries such as India, Brazil, and South Africa have argued that CBAM risks undermining the principle of Common but Differentiated Responsibilities under the UNFCCC and could disproportionately affect developing economies with carbon-intensive export sectors such as steel, aluminum, cement, and fertilizers.

Critics have also raised concerns regarding WTO compatibility, particularly around non-discrimination principles under the General Agreement on Tariffs and Trade (GATT), as well as the broader precedent such climate-linked trade measures could establish globally. For many countries in the Global South, these measures are increasingly viewed not only as climate instruments, but also as tools of industrial and geopolitical influence that could reshape future patterns of competitiveness, market access, and development space.

European policymakers and CBAM's defenders counter that the mechanism is an anti-leakage instrument rather than a trade barrier: because EU firms already pay for emissions under the ETS, CBAM merely places importers on an equal footing by charging the difference between the EU carbon price and any price paid at origin, and the EU argues that it has designed a non-discriminatory and WTO-compliant mechanism that attaches to embedded carbon content rather than nationality. On the CBDR objection specifically, the EU's response is that differentiation is built into the design rather than achieved through exemptions, since exporters can reduce or eliminate the levy by pricing carbon domestically an option that lets countries decarbonize at their own pace while preserving the incentive to act, and one that defenders note has already spurred carbon pricing around the globe.

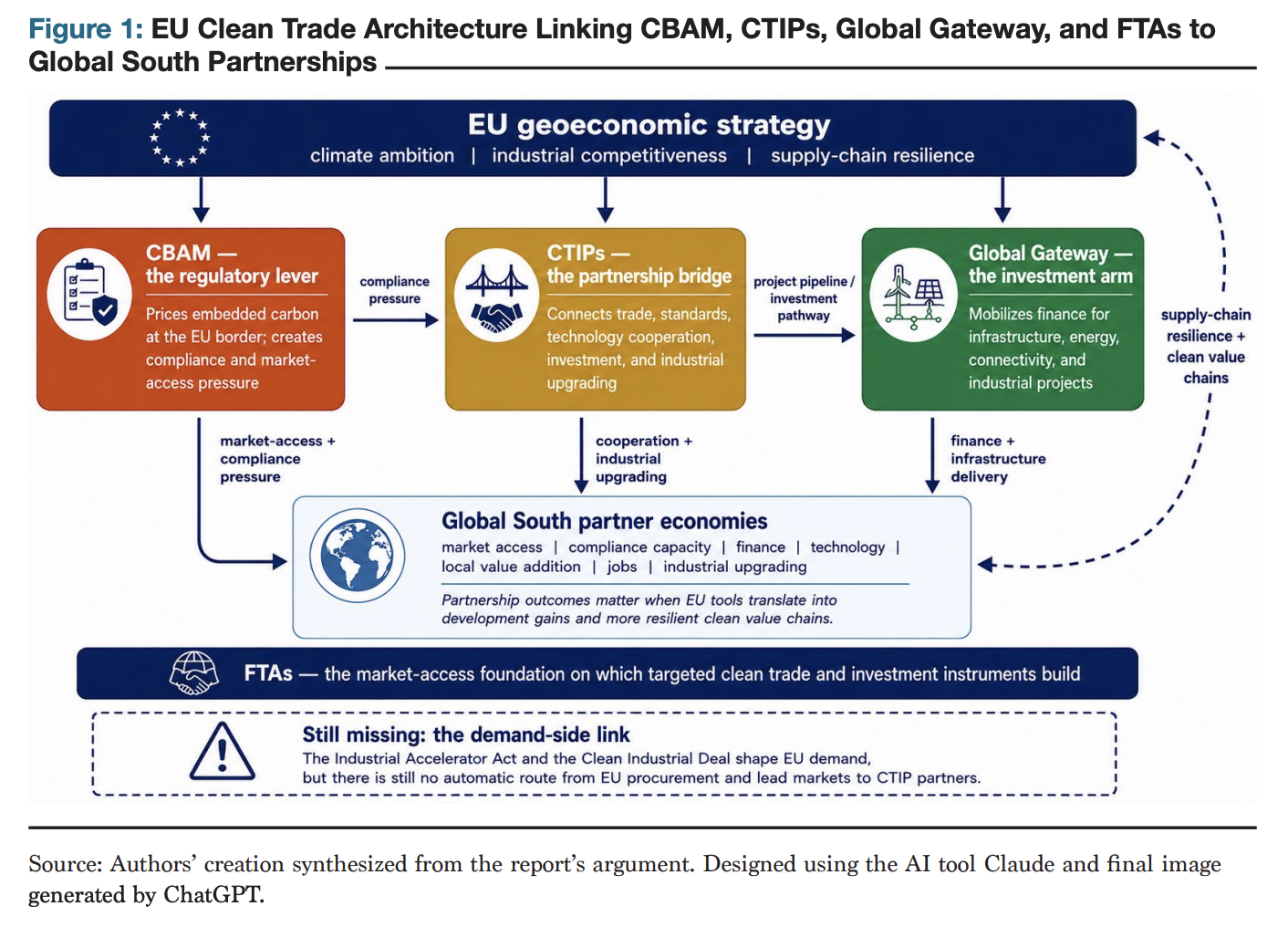

Where CBAM functions primarily as a regulatory instrument, Global Gateway and CTIPs have been framed by the EU as more cooperative mechanisms intended to support decarbonization through investment, industrial partnerships, and supply chain collaboration. Figure 1 presents an emerging and increasingly interconnected architecture, which better reflects the fact that CBAM, CTIPs, and Global Gateway were developed through different policy processes and are now being linked ex post. Launched in 2021, Global Gateway was presented as a strategic investment initiative aimed at mobilizing up to EUR 300 billion by 2027 across infrastructure, connectivity, digitalization, climate, and energy thematic areas. It has also been widely interpreted as Europe's response to China's Belt and Road Initiative, emphasizing transparency, sustainability, and rules-based cooperation. Climate and energy have been the largest sectoral focus of Global Gateway flagship projects in 2023-2024, accounting for roughly 49 percent of the total. The EU contributions to Just Energy Transition Partnerships (JETPs) in South Africa, Indonesia, Vietnam, and Senegal comprise a large share of these investments. Green hydrogen procurement and clean industrial value chains have become central pillars of this strategy, particularly where they align with Europe's long-term energy security and import diversification objectives.

At the same time, critics argue that some Global Gateway initiatives continue to prioritize European commercial and strategic interests over local industrial development priorities within partner countries. Concerns have also emerged around debt sustainability,

unequal bargaining power, and whether such partnerships risk reproducing extractive economic relationships under a green transition framework.

The rollout of the European Green Deal, including CBAM and Global Gateway, coincided with a period of major geopolitical and economic disruption, including the COVID-19 pandemic, Russia's invasion of Ukraine, growing U.S. industrial protectionism, and intensifying U.S.-China strategic competition. Together, these developments exposed vulnerabilities within Europe's energy systems, industrial supply chains, and economic model. In response, the EU has increasingly sought to recalibrate its external economic relationships, particularly with emerging economies that are central to future clean energy supply chains, industrial growth, and demand expansion.

This shift is also visible in the EU's renewed push to advance trade negotiations with key Global South partners, including India and the MERCOSUR countries, after years of stalled discussions. While these negotiations increasingly reflect broader Global Gateway priorities such as critical minerals, clean energy cooperation, and sustainability standards they have only partially addressed concerns surrounding CBAM and climate-related trade asymmetries. Technical dialogues and cooperation mechanisms have been introduced, but deeper tensions around competitiveness, equity, and compatibility with multilateral trade rules remains unresolved.

It is within this evolving geoeconomic landscape that CTIPs have begun to emerge. While CBAM seeks to enforce climate-related standards and Global Gateway focuses on mobilizing investment, CTIPs are being positioned as a more flexible and targeted mechanism capable of linking trade, investment, industrial cooperation, and supply chain resilience. In many ways, they represent the EU’s attempt to move beyond unilateral regulatory approaches toward more structured forms of clean industrial partnership with the Global South. Whether CTIPs can successfully bridge this gap and become genuinely co-created and mutually beneficial frameworks, rather than another layer of asymmetrical green conditionality, will depend largely on how they are designed and implemented in practice.

III. CTIPs: REIMAGINING CLEAN INDUSTRIAL COOPERATION

Against the backdrop of growing tensions between climate ambition, industrial competitiveness, and development concerns, the EU introduced CTIPs in 2025 as a more flexible and targeted framework for clean industrial cooperation with partner economies. CTIPs are designed to encourage regulatory dialogue, alignment on industrial decarbonization pathways, cooperation on carbon pricing, CBAM readiness, and Monitoring, Reporting, and Verification (MRV) systems, and to support market access and early-stage industrial policy coordination. Unlike FTAs, CTIPs are intended to be targeted, sector-specific, and tailored to partner-country priorities, allowing for faster and more flexible cooperation around strategic clean energy value chains. Together with Global Gateway and CBAM, CTIPs represent a measure that ultimately falls under the broader strategic objective of supporting global energy transitions while also securing resilient supply chains and industrial competitiveness for the EU.

The stated objectives of CTIPs are broadly threefold:

Secure resilient supply chains: Diversifying sources of critical raw materials, clean technologies, and industrial inputs required for the EU's energy transition goals.

Support green industrialization: Moving beyond extractive economic models toward greater local value creation and low-carbon manufacturing in partner economies.

Enable execution and investment certainty: Addressing implementation bottlenecks such as permitting delays, lack of grid readiness, standards fragmentation, and regulatory uncertainty while helping create more bankable and investable industrial ecosystems.

These objectives reflect a broader shift toward what can be described as "green comparative advantage," where industrial production is increasingly shaped not only by labor costs or market proximity, but also by access to clean energy, lower carbon intensity, availability of critical minerals, and resilient supply chains. In this sense, CTIPs represent an attempt to align climate ambition with industrial strategy and geoeconomic resilience.

At the same time, whether CTIPs can genuinely support green industrialization, technology access, and climate finance mobilization in the Global South, rather than simply introducing new layers of compliance obligations and trade conditionality, remains an open question. The risk is particularly acute if partnerships raise adjustment costs for developing economies without providing adequate financing, technology cooperation, or realistic transition timelines.

Nowhere is this tension more visible than in critical minerals cooperation, which will be one of the clearest tests of whether CTIPs can avoid reproducing older extractive patterns of North-South economic engagement. For many resource-rich countries, the central concern is that the energy transition could reinforce a familiar division of labor in which raw materials are exported while processing, manufacturing, technology development, and higher-value industrial activity remain concentrated elsewhere. CTIPs will therefore need to link critical minerals diplomacy to downstream processing, local manufacturing, decent jobs, skills development, technology upgrading, and domestic value retention. This, in turn, will require significant infrastructure investments in partner countries to support these projects and allow the absorption of relevant tech transfer to increase the CTIPs equitability to countries in the Global South.

For many Global South countries, the success of CTIPs will therefore depend less on political declarations and more on whether they are accompanied by tangible delivery mechanisms, including concessional finance, industrial investment, skills partnerships, and technology collaboration. In this regard, delivery-oriented instruments such as Global Gateway will likely need to function in tandem with CTIPs for the framework to be viewed as a credible enabler rather than simply another regulatory layer. A careful balance will need to be struck for the EU to ensure that CTIPs are genuinely mutually beneficial, supporting global resilience and industrial development while also advancing Europe's own economic and strategic interests.

In practice, CTIPs are neither tariff-cutting agreements nor direct financing mechanisms. Rather, they sit alongside existing trade, industrial, and investment frameworks and place greater emphasis on strategic sectors such as clean technology value chains, critical raw materials, industrial decarbonization, standards cooperation, and workforce development. This hybrid positioning is important because it allows CTIPs to operate at the intersection of trade policy, industrial strategy, and climate diplomacy without requiring the lengthy negotiation timelines associated with comprehensive FTAs.

For the Global South, the framing of CTIPs as voluntary, co-designed, and co-implemented partnerships is particularly important in the context of regulatory instruments such as CBAM and investment initiatives like Global Gateway, which are often perceived as asymmetric in both design and implementation. In 2022, the BASIC countries (Brazil, South Africa, India, and China) stressed that "unilateral measures and discriminatory practices, such as carbon border taxes, that could result in market distortion and aggravate the trust deficit amongst parties, must be avoided." This reflects a wider concern that the challenge lies not only in the design of CTIPs themselves, but in the cumulative effect of the EU's broader climate-trade architecture. Instruments such as CBAM, EUDR, sustainability taxonomies, and evolving standards frameworks are increasingly viewed by some actors as a potential form of "green conditionality," particularly where they raise compliance costs or narrow industrial policy space without commensurate finance, technology access, or market opportunities. From this perspective, CTIPs will need to demonstrate that they are not simply a softer extension of unilateral regulatory externalization, but genuinely co-created industrial partnerships that support diversification, local value creation, and movement up clean value chains.

The credibility of CTIPs will therefore depend heavily on whether partner countries see tangible economic value in participation, including opportunities for domestic manufacturing, local job creation, technology upgrading, and integration into emerging clean industrial value chains. Their long-term viability will in turn depend on complementary finance, access to technology, policy flexibility, and credible transition timeframes that account for differing national development realities.

The South Africa CTIP, announced in 2025, was a strategic first choice for the EU given South Africa's critical mineral resource endowments, existing green industrial base, significant Global Gateway-linked investments through the JETP, and growing industrial decarbonization needs. Recent announcements around the pilot have reiterated broader CTIP objectives, and aligned them with South Africa's long-standing ambitions to decarbonize its economy and move beyond raw material exports toward greater domestic manufacturing and value addition. For Global South countries, this pilot will illustrate both the promise and the risks associated with CTIPs. For the EU, it will test whether such partnerships can move beyond perceptions of green protectionism and evolve into credible platforms for industrial cooperation with manageable costs and shared economic benefit.

IV. THE GLOBAL SOUTH: PERSPECTIVES AND EXPECTATIONS

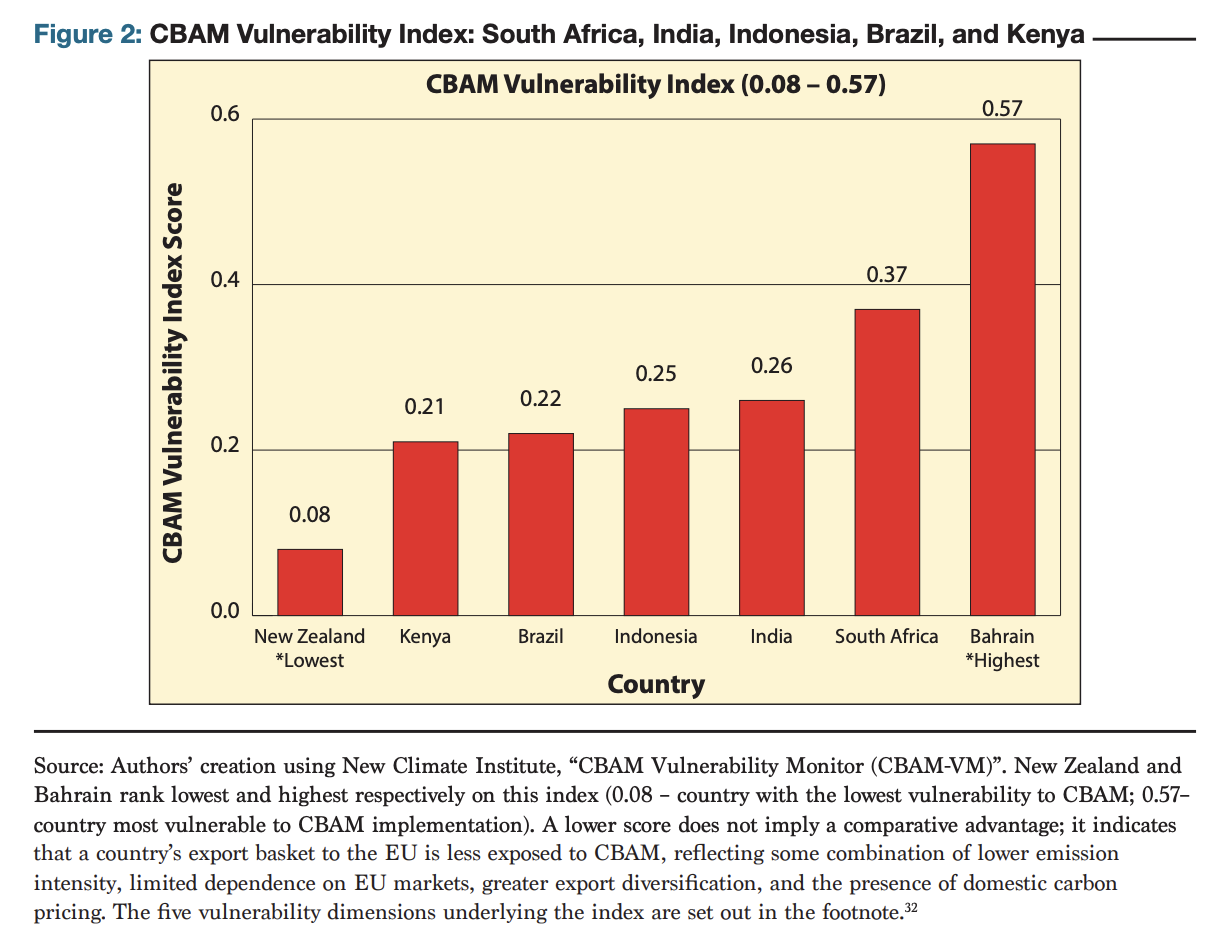

Across key prospective CTIP partners, major export-oriented industries such as steel, aluminum, fertilizers, mining, and agro-processing are increasingly exposed to evolving EU climate and sustainability regulations, particularly the CBAM. While CBAM is intended to reduce carbon leakage and protect the competitiveness of European industry, its impact across the Global South is highly uneven. Vulnerability depends not only on the carbon intensity of Global South exports to the EU, but also on factors such as dependence on EU markets, export concentration, industrial diversification, domestic carbon pricing systems, and institutional readiness for MRV requirements. For many developing economies, the challenge is therefore not only decarbonization itself, but also the administrative, technological, and financial capacity required to comply with emerging climate-linked trade regimes.

Figure 2 illustrates the relative CBAM vulnerability of five countries: South Africa, India, Indonesia, Brazil, and Kenya, which together represent a diverse cross-section of prospective Global South CTIP partners. These countries were selected because they reflect different economic structures, industrial capabilities, export profiles, and strategic interests in relation to the EU. South Africa represents a carbon‑intensive industrial economy with significant dependence on coal‑based power and mineral exports, and is a JETP country. India represents a large industrializing economy highly exposed to EU climate–trade measures through steel and manufacturing exports. Indonesia is central to global critical mineral and battery supply chains. Brazil combines agricultural, mining, and clean energy export ambitions. Kenya illustrates smaller emerging economies where exposure to EU standards, and constraints on standards readiness and compliance capacity, are often more important than industrial emissions themselves. Together, they demonstrate the varying opportunities, expectations, and vulnerabilities shaping Global South perspectives on CTIPs.

As Figure 2 demonstrates, South Africa emerges as the most vulnerable among the five countries analyzed, reflecting its carbon-intensive industrial base, export exposure, and limited diversification in affected sectors. Vulnerability to CBAM is further exacerbated by the absence or limited maturity of domestic MRV systems and carbon accounting frameworks that are increasingly necessary for maintaining market access under evolving EU regulations. This is precisely where CTIPs could play a critical role — not simply as trade frameworks, but as enabling platforms for regulatory cooperation, MRV readiness, industrial upgrading, technology access, and investment mobilization. Whether CTIPS succeed in fulfilling that role, however, will depend heavily on how partner countries perceive their fairness, flexibility, and developmental value.

South Africa

Speaking at an ORF America event on CTIPs in Brussels on April 22, 2026, a South African government representative stated that South Africa had entered into the CTIP on the basis that it would be a "partnership of equals" centered on mutual beneficiation. It seeks for its newly agreed CTIP to prioritize local value addition, technology transfer, and skills development, enabling domestic firms to move up clean value chains rather than remain primarily raw-material exporters. Recognition of South Africa's national decarbonization and reporting frameworks, together with EU support for MRV readiness and industrial decarbonization finance, will be important for ensuring that CTIPs support both competitiveness and climate ambition rather than becoming another layer of regulatory burden.

Key priorities include expanding grid capacity and enabling greater renewable energy integration, alongside supporting the transformation of carbon-intensive industries such as SASOL, an integrated energy and chemical company, toward lower-carbon production pathways, including sustainable aviation fuels (SAFs). From South Africa's perspective, CTIPs are viable only if they function as platforms for co-development, industrial upgrading, and long-term investment, aligning EU climate objectives with South Africa's broader goals of job creation, energy transition, and structural economic transformation.

South Africa's CTIP should also be viewed against a broader African industrialization context, including regional ambitions under Agenda 2063, the African Continental Free Trade Area (AFCFTA), and emerging continental debates around green minerals strategy, mutual beneficiation, and regional value chains. This matters because CTIPs with African partners will be assessed not only bilaterally, but also in light of whether they support wider African goals of industrial diversification, intra-regional value addition, and economic transformation.

India

For India, long-standing sensitivities around the regulatory conditionalities embedded within EU trade agreements contributed to delays in FTA negotiations for nearly two decades. While the EU-India FTA negotiations concluded in early 2026, CBAM remains a central concern. The EU accounts for approximately 17 percent of India's goods exports and over 60 percent of India's steel exports, leaving India particularly exposed to EU carbon pricing benchmarks (Figure 1).

For India, a CTIPs could offer a useful sector-specific bridge, particularly for hard-to-abate sectors such as steel that are likely to be significantly affected by CBAM. From India's perspective, any meaningful partnership would need to go beyond compliance and support domestic industrial transformation through climate finance mobilization, technology cooperation, and market certainty. India is seeking financial and technological support for emerging sectors such as green hydrogen and green steel, alongside credible and interoperable EU certification systems. Affordable access to technology and support in lowering the high cost of capital, particularly for micro, small, and medium-sized enterprises (MSMEs), remain critical priorities. Specific supply chain gaps, such as cold rolled steel for transformers, also remain strategically important.

The EU-India FTA includes proposals for technical dialogues on CBAM and provisions around Most-Favored-Nation (MFN) treatment during implementation, which represent important confidence-building measures. Alongside these transitional arrangements, recognition of domestic Indian schemes such as the Perform, Achieve and Trade (PAT) mechanism and the Indian Carbon Market framework (ICM-CCTS) will be critical for building credible MRV cooperation and avoiding duplicative compliance systems.

However, long-term CBAM compliance will ultimately require deeper industrial and technological partnerships capable of building domestic low-carbon manufacturing capacity at scale. In this regard, the EU-India Trade and Technology Council's cooperation framework on semiconductors offers a potentially useful model for how both sides could collaborate on industrial decarbonization and strategic clean technology ecosystems. A CTIP tailored to India's needs, combining short-term MRV and standards support with longer-term climate finance, industrial and infrastructure investment, and technology partnerships, has a strong chance of success.

Indonesia

Similarly, Indonesia is a natural candidate for CTIPs, although its engagement with the EU has been shaped by longstanding frictions over sustainability-linked trade measures — from palm-oil and biofuel disputes to newer instruments such as CBAM and the EU De-forestation Regulation (EUDR) — which Indonesian officials and stakeholders frequently criticize as unilateral and insufficiently sensitive to developing country conditions. As the world's largest nickel producer, accounting for over 53 percent of global nickel production and 42 percent of reserves, Indonesia is central to the future of global battery and electric vehicle supply chains. This gives Indonesia significant strategic leverage in the emerging clean energy economy, particularly as countries seek to diversify critical mineral supply chains.

At present, Indonesia's nickel processing and smelting ecosystem is heavily influenced by Chinese investment, and the country is actively seeking to diversify its industrial and investment partnerships. Rather than remaining simply a supplier of raw materials, Indonesia's broader ambition is to move up the clean energy and minerals value chain into higher value manufacturing, including batteries, electric vehicles, and downstream clean energy industries. In this context, an EU-Indonesia CTIP would need to focus not only on market access and standards alignment, but also on connective infrastructure, industrial capacity building, technology cooperation, and long-term investment in domestic manufacturing ecosystems.

To ensure Indonesian firms remain competitive in European markets, recognition of interoperability between EU and Indonesian sustainability, traceability, and certification systems will be critical for building credible MRV cooperation. Indonesia is seeking to co-develop standards that are internationally credible and acceptable to the EU, but not prohibitively expensive or administratively burdensome for domestic producers to implement. This reflects a broader concern across many Global South economies that fragmented or overlapping sustainability regimes could increase compliance costs and create new barriers to participation in clean industrial value chains.

Whereas India's interest in CTIPs is shaped primarily by CBAM exposure in industrial sectors such as steel, Indonesia's priorities are more closely tied to critical minerals, downstream manufacturing, and standards interoperability. As a result, Indonesia would likely favor a CTIP framework that supports industrial upgrading, avoids duplicative certification systems, and enables greater participation in higher-value clean technology supply chains.

Brazil

With renewed political momentum around the EU-Mercosur trade agreement and Brazil's ambition to position itself as a global clean energy and bioeconomy powerhouse, the country is well positioned for CTIPs. Brazil's perspective is shaped by its dual identity as a major exporter of both industrial and agricultural commodities, while also emerging as a potential leader in low-carbon fuels and nature-based industries. The EU accounts for approximately 16 percent of Brazil's goods exports, including iron ore, steel inputs, soy, and biofuels, sectors increasingly exposed to evolving EU climate and sustainability regulations such as CBAM and the EUDR.

At the same time, Brazil is likely to approach CTIPs with a strong emphasis on preserving policy autonomy and ensuring recognition of domestic regulatory systems, particularly around climate governance, land use, and traceability frameworks. From Brazil's perspective, interoperability and mutual recognition are likely to be more politically acceptable than the creation of parallel EU-led compliance systems.

As Brazil positions itself as a global leader in green hydrogen, SAFs, biofuels, and broader bio-based industries, a tailored CTIP framework that supports technology cooperation, market access, investment flows, and long-term offtake arrangements could deliver meaningful gains for both sides. For the EU, Brazil offers access to large-scale clean energy potential and low-carbon industrial inputs. For Brazil, CTIPs could help accelerate industrial upgrading and integration into emerging global clean energy value chains.

Kenya

For countries such as Kenya, the CTIP calculus is different from that of larger industrial economies. Kenya's primary challenge is not large-scale industrial decarbonization, but rather standards readiness, certification capacity, and the high administrative cost of compliance, particularly in agro-processing, agriculture, and light manufacturing sectors. While larger economies are more directly exposed to measures such as CBAM, Kenya's experience illustrates how smaller developing economies are increasingly affected by climate-linked trade governance through sustainability standards, traceability requirements, and compliance systems tied to market access. The EU absorbs approximately 14 percent of Kenya's goods exports, and emerging EU sustainability regulations risk introducing reporting and traceability burdens that can disproportionately affect smaller exporters and firms with limited technical capacity. 52 In many cases, the challenge is less about reducing emissions and more about navigating increasingly complex regulatory systems tied to market access.

The EU-Kenya Economic Partnership Agreement (EPA) already provides duty-free and quota-free access for Kenyan exports, alongside safeguards for Kenya's developing industries. In this context, a possible CTIP would be less about reopening tariff negotiations and more about deepening economic integration through standards cooperation, certification support, and industrial upgrading. For Kenya, the value of a CTIP would likely depend on whether it can simplify compliance processes, strengthen domestic certification ecosystems, and help smaller firms participate more competitively in emerging green value chains.

Guaranteed market access, simplified rules-of-origin procedures, interoperable certification systems, and targeted technical assistance for clean industry development would therefore be among the most important outcomes of a potential EU-Kenya CTIP. Kenya also highlights an important broader lesson for CTIPs: not all partner countries will engage these frameworks primarily through heavy industry, critical minerals, or carbon pricing exposure. For many smaller developing economies, the biggest barriers to participation in green trade are often institutional and administrative rather than technological alone.

Collectively, the experiences of India, Brazil, South Africa, Indonesia, and Kenya underscore that the success of CTIPs will depend less on their design as flexible trade instruments and more on whether they can bridge the gap between EU regulatory ambition and partner-country development priorities. Across partners, this pattern is consistent. India seeks MRV recognition and sectoral support for green steel, Indonesia prioritizes standards interoperability and downstream industrialization, and Brazil emphasizes policy autonomy alongside market access. In the same vein, South Africa requires scaled finance, localization, and industrial upgrading, and Kenya needs simplified compliance systems that translate preferential market access into competitiveness.

Concurrently, experience with previous EU-led climate and energy initiatives highlights a recurring gap between political announcements and the timely mobilization of finance, project execution, and institutional delivery. Lengthy approval procedures, overlapping governance structures, and fragmented financing channels risk undermining CTIPs' ability to respond at the speed and scale partners require.

Without credible commitments on mutual recognition, finance, technology cooperation, market access, streamlined procedures, and reduction of administrative burdens, CTIPs risk being perceived as extensions of unilateral EU climate measures rather than platforms for co-development, economic rebalancing, and equitable industrial transformation. That perception would carry strategic costs. Competing providers of infrastructure and industrial finance can offer speed, scale, and minimal conditionality, and may prove more attractive even though the EU brings a stronger underlying offer: privileged access to the world's largest single market, an emphasis on local value addition over raw-material extraction, deeper technology transfer and skills development, and blended finance that lowers the cost of capital while safeguarding debt sustainability and environmental standards. The EU’s challenge is less the quality of its offer and more so its ability to deliver quickly, predictably, and with genuine reciprocity.

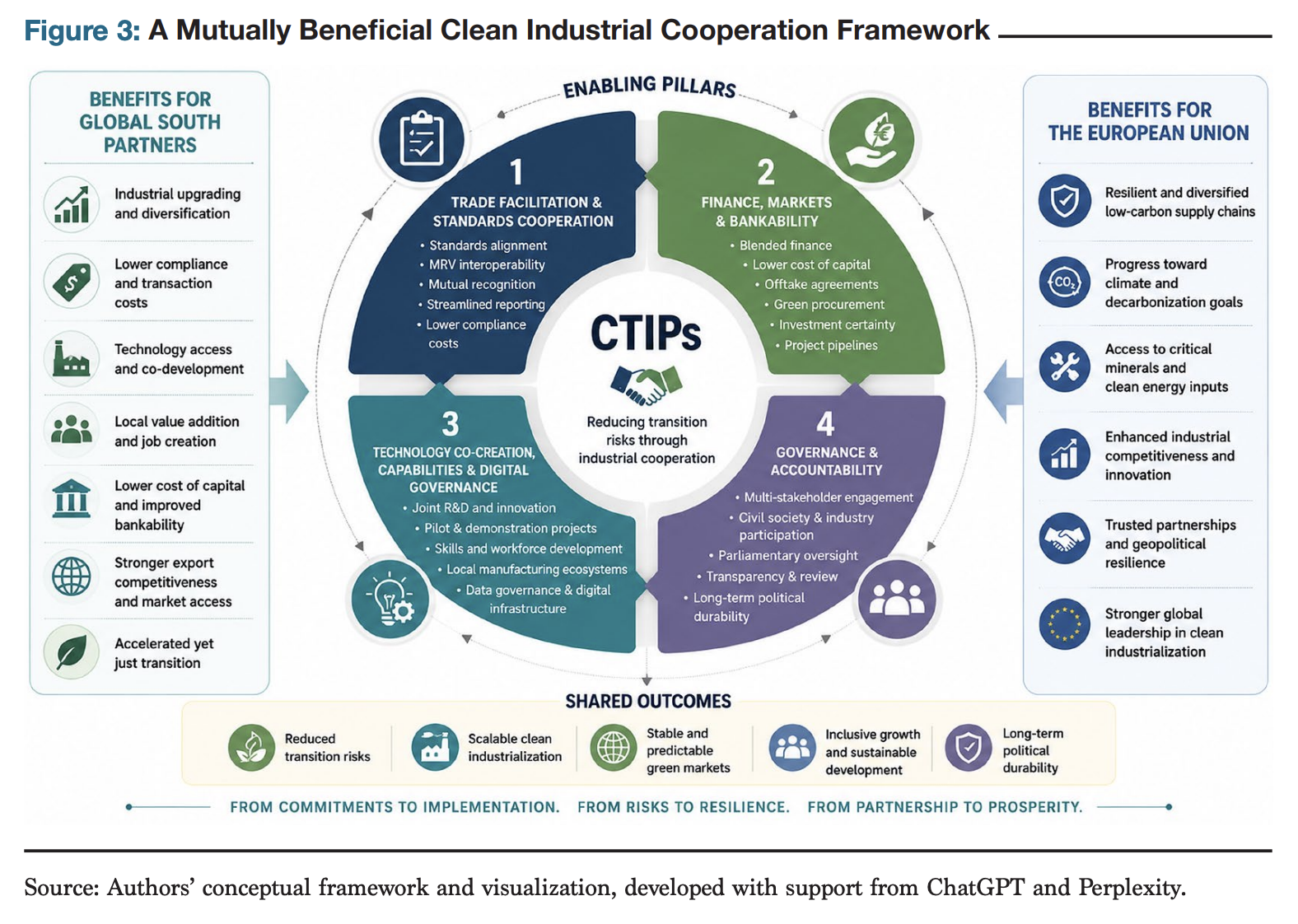

V. OPERATIONALIZING MUTUALLY BENEFICIAL CTIPS

The diverse expectations of Global South partners demonstrate that CTIPs cannot function as a one-size-fits-all trade arrangement architecture or compliance-focused framework. Their long-term credibility will depend on whether they can evolve into practical platforms for industrial cooperation that align trade facilitation, finance, technology partnerships, and governance mechanisms around shared transition priorities. In practice, the value of CTIPs may lie less in traditional trade liberalization and more in their ability to reduce the multiple layers of risk that constrain clean industrial investment across emerging economies, including regulatory uncertainty, fragmented standards, high financing costs, technology access barriers, and weak implementation capacity.

This requires CTIPs to operate not simply as outlining ambitions for partnership, but as implementation-oriented frameworks that integrate regulatory cooperation, investment, infrastructure, and industrial strategy around a limited number of priority sectors. In many ways, this mirrors the EU's own experience under the European Green Deal, where regulation, finance, industrial policy, and infrastructure planning have been pursued in an integrated manner rather than as isolated policy tools. Rather than pursuing broad and diffuse cooperation agendas, CTIPs are likely to be most effective when structured around sector specific industrial ecosystems where standards cooperation, infrastructure, finance, market access, and technology partnerships reinforce one another.

To translate CTIPs from political concepts into workable and mutually beneficial partnerships, several enabling pillars will be critical (see Figure 3). These include trade facilitation, financing, execution and demand creation, technology co-development, and governance frameworks that together can reduce implementation risks and support long-term industrial transformation.

Trade facilitation should ideally serve as the entry point for CTIPs tailored to emerging economies. The need to reduce the transaction and compliance costs associated with existing EU climate-linked trade measures has been consistently emphasized by countries with high vulnerability to instruments such as CBAM. Instead of imposing bilateral "EU-only" standards, CTIPs should prioritize alignment with international standards frameworks such as ISO and IEC systems. Mutual recognition or equivalence pathways for emissions MRV systems, alongside the digitalization and streamlining of reporting systems, can improve interoperability and reduce administrative burdens for partner firms while giving EU regulators more consistent, comparable data.

Importantly, for many Global South economies, the challenge is not opposition to climate standards themselves, but the cost, complexity, and fragmentation associated with multiple overlapping compliance regimes. Transitional arrangements that account for

different levels of industrial development and sector-specific decarbonization timelines can create more realistic pathways for emissions reductions while maintaining competitiveness. By prioritizing facilitation, interoperability, and administrative simplification over purely unilateral enforcement, CTIPs can help prevent sustainability standards from functioning as de facto trade barriers and instead turn them into instruments that support export upgrades and more predictable market access for partners, while improving the reliability and resilience of the EU's low-carbon supply chains. Several common threads run through these facilitation measures and connect directly to the partner priorities identified above: lowering the cost of capital associated with CBAM alignment, enabling mutual learning on the design and implementation of environmental standards, and supporting the development of domestic carbon markets including emissions trading systems — which can give many Global South economies an effective domestic price signal and a credible foundation for MRV cooperation.

FINANCE, MARKETS, AND BANKABILITY

Without access to affordable and appropriately structured finance, trade facilitation alone will be insufficient. CTIPs should therefore serve as enabling frameworks that help align EU public finance, multilateral development banks, private capital, export credit agencies, and Global Gateway investments around shared industrial transition priorities. Rather than functioning solely as investment pipelines, CTIPs can add value by focusing on the enabling conditions required for clean industrial transformation, including grid infrastructure, permitting systems, MRV readiness, industrial clustering, and long-term policy certainty. For partners, this alignment can lower the cost of capital, expand access to long-term project finance, and support domestic value addition and job creation. For the EU, this linkage underpins more resilient and diversified low-carbon supply chains.

However, capital flows only where there is demand certainty. CTIPs can help create lead markets through long-term offtake agreements, green public procurement, advance purchase commitments, and certification alignment. A more explicit focus on risk allocation will also be necessary. Many CTIP-aligned projects in emerging markets will struggle to reach financial close unless partners clearly identify who absorbs early-stage transition risks, including currency risk, political risk, demand uncertainty, technology risk, and first-mover costs. CTIPs should also acknowledge the structural competitiveness asymmetries created by differing subsidy regimes. EU Green Deal subsidies, the U.S. Inflation Reduction Act, and Chinese industrial policy support have intensified concerns that developing economies are being asked to compete in clean industrial sectors without comparable fiscal space. CTIPs cannot resolve these asymmetries on their own, but they can partially offset them by linking regulatory cooperation to scaled industrial finance, concessional support, demand creation, and credible access to EU clean industrial markets.

A sector-specific opportunity such as an EU-India green hydrogen partnership could serve as an important model for industrial decarbonization cooperation. India's National Green Hydrogen Mission aims to position the country as a major producer and exporter, while the EU's hydrogen strategy anticipates substantial import dependence to meet long-term decarbonization targets, creating a natural basis for strategic alignment. Through CTIPs, this cooperation could move beyond political dialogue to enable joint standards-setting, certification interoperability, infrastructure coordination, and long-term offtake arrangements that are essential for de-risking investment. Such an approach would recognize that the principal constraint facing many Global South economies is often not the lack of decarbonization ambition, but the high cost of capital and limited investment certainty surrounding emerging green industries. By lowering these risks and improving long-term visibility, CTIPs could help accelerate the bankability and deployment of clean industrial projects at scale, while giving the EU credible access to future clean energy and materials supplies.

TECHNOLOGY CO-CREATION, CAPABILITIES, AND DIGITAL GOVERNANCE

For many emerging economies, domestic capability-building, skills development, and licensing pathways are just as important as affordable technology access itself. These elements are essential for ensuring the long-term sustainability and competitiveness of clean industries while avoiding new forms of technological dependence. Technology access alone is therefore unlikely to be sufficient. CTIPs should also support the "missing middle" of innovation, particularly in the Technology Readiness Level (TRL) 4-7 range, where demonstration, prototyping, validation, and scale-up occur, but financing and institutional support are often limited. In practical terms, this means supporting collaborative research and development, pilot and demonstration projects, and investing in institutional arrangements that bring together governments, firms, and universities in "triple-helix" style innovation ecosystems. In this sense, successful CTIPs should help partner countries participate in innovation ecosystems, develop domestic manufacturing capabilities, contribute to standards-setting processes, strengthen local supplier networks, and build workforce capabilities, rather than simply improving access to imported technologies.

In industrial decarbonization and clean manufacturing sectors, CTIPs can facilitate co-development arrangements that allow partner countries to adapt technologies to local industrial conditions and enable gradually building domestic manufacturing, operational, and maintenance capacity. This shift from technology transfer toward technology co-creation is likely to be critical for building long-term trust and political legitimacy within Global South partner countries, while giving the EU more reliable innovation partners and stable cost-effective low-carbon production bases.

CTIPs should also include clearer frameworks around data governance and digital infrastructure, particularly in increasingly digitized energy and industrial systems. Building on the standards and MRV cooperation set out in the trade facilitation pillar, ensuring transparency around data ownership, access, and usage rights will become increasingly important as countries seek to balance clean industrial cooperation with broader concerns around digital sovereignty and strategic technological autonomy. This can help prevent the emergence of new technological dependencies or concentrated "monopolies of capability" within future clean energy ecosystems and reassure partners that digital and industrial cooperation does not come at the expense of their strategic autonomy or the space for domestic innovators to develop and deploy their own solutions.

GOVERNANCE AND DEMOCRATIC SCRUTINY

To ensure long-term stability and political legitimacy, CTIPs will require robust governance structures that extend beyond government-to-government engagement alone. Domestic advisory groups, bringing together civil society, industry, trade unions and other independent stakeholders, can provide an institutionalized channel can provide an institutionalized channel for stakeholders to advise on implementation and raise sustainability-related concerns about how the agreement is applied in practice, rather than being limited to commenting on a narrow set of "sustainability" provisions. Multi-stakeholder governance of this kind can also generate more granular information on sector- and region-specific impacts, helping policymakers identify concrete project opportunities and bottlenecks on the ground and translate high-level commitments into implementable pipelines.

Such governance mechanisms are particularly important given that CTIPs sit at the intersection of trade, climate, industry, and development policy, areas that increasingly shape domestic political and economic priorities. Operationalizing parliamentary engagement, civil society participation, and transparent review mechanisms will therefore be essential for accountability, trust-building, and long-term stakeholder buy-in. Without credible governance arrangements, even well-designed CTIPs risk facing political resistance, implementation delays, or perceptions of asymmetrical decision-making. Conversely, where partners see that governance arrangements allow them to shape priorities, scrutinize outcomes, and adjust course, CTIPs are more likely to be perceived as genuinely mutual partnerships rather than externally driven instruments.

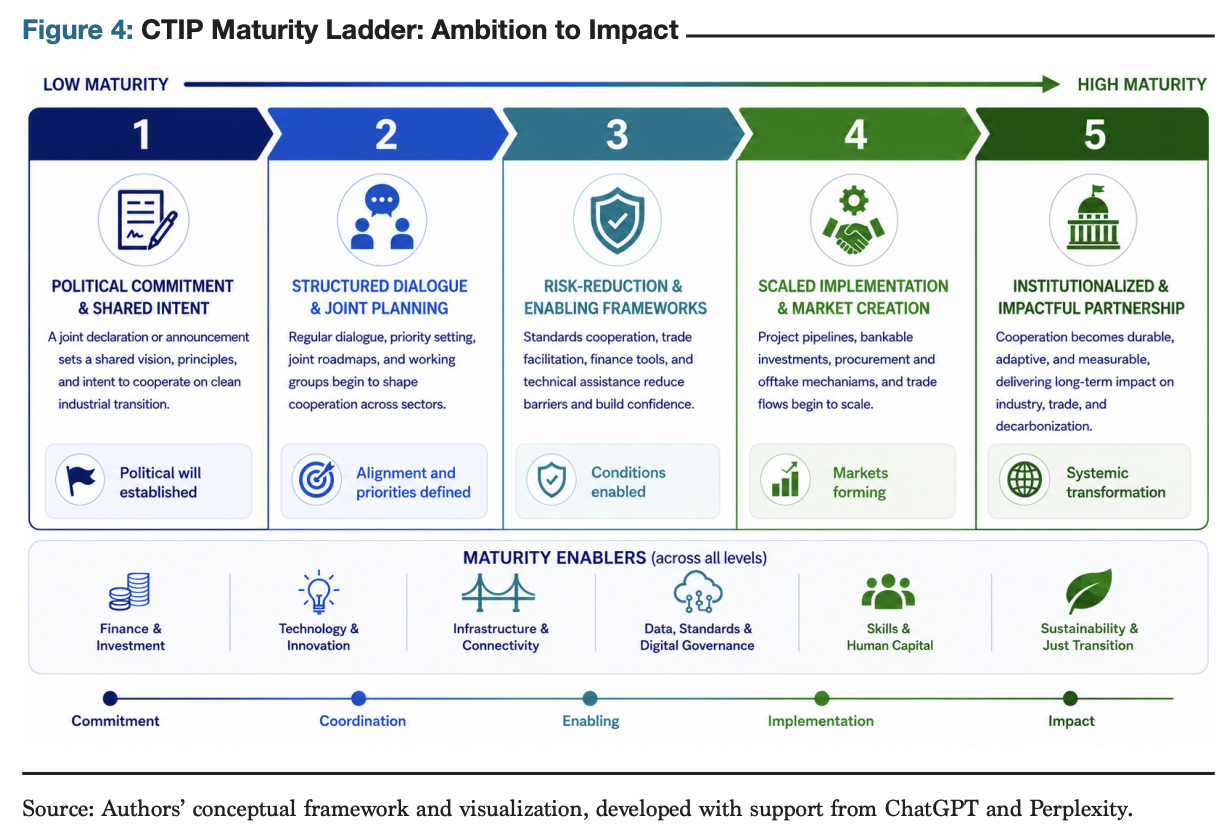

While these principles provide a broader framework for making CTIPs more effective and credible, implementation will ultimately depend on how well partnerships are adapted to the realities of different economies and industrial sectors as well as future global economic growth prospects. Large industrial economies may prioritize hard to abate sectors such as steel, cement, or chemicals, while smaller and lower income economies may focus more on standards readiness, certification capacity, renewable energy deployment, or green manufacturing opportunities. In this context, it may be useful to view CTIPs through a "maturity ladder," where partnerships evolve progressively from political declarations and dialogue mechanisms toward risk reduction frameworks, bankable project pipelines, and eventually embedded governance and long-term industrial cooperation.

As shown in Figure 4, this maturity ladder can also be used as a diagnostic tool for assessing CTIP progress over time. At Levels 1-2, the political-dialogue phase, CTIPs establish shared priorities and consultation channels but remain largely diplomatic. At Level 3, the implementation phase, CTIPs begin addressing standards, MRV, certification, permitting, and regulatory bottlenecks through concrete cooperation instruments.

At Level 4, the investment phase, CTIPs connect these reforms to bankable project pipelines, concessional finance, offtake arrangements, and demand‑creation tools. At Level 5, the integrated industrial‑ecosystem phase, CTIPs support long‑term value‑chain integration through local manufacturing, skills development, technology co‑creation, regional value chains, and embedded governance mechanisms.

Such a framework highlights that CTIPs become more credible and mutually beneficial as they move from ambition toward implementation, institutionalization, and measurable outcomes. The long-term success of CTIPs will therefore depend not only on regulatory alignment, but on their ability to translate cooperation into tangible industrial, financial, and developmental outcomes for both the EU and partner countries.

VI. THE WAY FORWARD

The most valuable contribution of the coming period will be to show, through a small number of visible wins, that cooperation can move at the speed and scale partners actually need, while responding to differing transition priorities and development pathways. In the immediate term, the most low-friction first steps in such cooperation include common or interoperable joint MRV and standards systems and a handful of de-risking projects in priority sectors such as green steel, hydrogen, and critical minerals. These initiatives should be designed not only to mobilize investment, but also to demonstrate that CTIPs can translate political intent into practical outcomes. Closing the demonstration gap between ambition and implementation could create a powerful signaling effect, showing that countries with different histories and capabilities can make real progress on shared goals. Over the medium term, these confidence-building measures can mature into deeper partnerships: co-invested innovation clusters, interoperable data-sharing and certification systems, and technology co-creation partnerships that build lasting capability rather than dependence, supported by blended finance arrangements, joint research, demonstration projects, skills development, and local manufacturing ecosystems. Designed with sufficient institutional safeguards, transparency, and accountability mechanisms, these partnerships can help build the trust necessary for long-term cooperation, with both sides managing commitments and benefits at each stage.

Attempted this way, CTIPs are not a long list of aspirations or standalone agreements, and their promise lies in recognizing that mutual benefit is neither automatic nor uniform. The underlying conditions are unusually favorable. The EU needs resilient, lower-carbon supply chains and the Global South seeks investment, technology, and project delivery. Meanwhile, the climate challenge requires countries to move forward together rather than apart. If the EU and its partners treat these early arrangements as genuine co-creation rather than transactional bargains, CTIPs can become more than just another instrument in a crowded toolbox. They can become a working model of how climate ambition, industrial competitiveness, and economic development can reinforce one another through partnerships that create tangible value for all sides in a more cooperative global economy.

ACKNOWLEDGMENTS

The authors are grateful to the participants of the day-long international EU-Global South dialogue on Clean Trade and Investment Partnerships held in Brussels on April 22, 2026, for their valuable insights and contributions. They also extend their thanks to Caroline Arkalji (ORF America) for her research and convening support.

This paper benefited from a thoughtful review and feedback from Dr. Raul Alfaro-Pelico, Senior Fellow at Lancaster University and G20 Senior Advisor to the African Union; Camille Boullenois, Associate Director at Rhodium Group; Paul Butarbutar, Executive Director of the Indonesia Climate and Growth Dialogue; Kęstutis Kupšys, Alternate Member of the European Economic and Social Committee; Seutame Maimele, Economist: Sustainable Growth at Trade and Industrial Policy Strategies; Tirthankar Mandal, Associate Director – Energy at WRI India; Máximo Miccinilli, Senior Vice President and Head of Energy, Climate and Mobility, FleishmanHillard EU; Dr. Chantelle Moyo, Just Transition Lead, Southern Transitions; and Dr. Chigozie Nweke-Eze, Postdoctoral Research Associate at Oxford Net Zero, University of Oxford. The authors are also thankful to Jeffrey D. Bean for edits of this paper. Every effort has been made to ensure the accuracy of the information and analysis presented in this paper. Any remaining errors or omissions are unintentional and remain the sole responsibility of the authors.

The authors also gratefully acknowledge the support of the Sequoia Climate Foundation.

Cover image created by Medha Prasanna using ChatGPT image generation, OpenAI, 2026.

Note: Citations and references can be found in the PDF version of this paper available here.